Skip to content

Skip to content

Ed Parsons CPA | IRS Tax Resolution and Collections Defense

A CP40 notice means the IRS has assigned your unpaid federal tax debt to a private collection agency (PCA). The IRS no longer manages direct collection on your account. Instead, an approved third-party company will contact you by letter and phone to collect the balance owed on behalf of the IRS.

Receiving a CP40 notice can feel alarming, especially if you did not expect to hear from anyone other than the IRS. This guide explains exactly what the notice means, which companies are authorized to contact you, what your rights are, and when to involve a tax professional before responding.

What Is a CP40 Notice?

The CP40 is an official IRS notice informing a taxpayer that their account has been transferred to the IRS Private Debt Collection (PDC) program. The IRS launched this program under the Fixing America’s Surface Transportation (FAST) Act, which requires the IRS to use approved private collection agencies for certain categories of overdue tax accounts.

The notice arrives by mail and includes the name of the assigned collection agency, a unique authentication number, and instructions on how to verify the contact is legitimate.

Why Did the IRS Send Your Account to a Debt Collector?

The IRS transfers accounts to private collectors when specific conditions are met. Your account likely qualified because it falls into one of the following categories:

| Reason for Transfer | What It Means |

| Inactive IRS inventory | The IRS has not actively worked your account in a significant period |

| IRS lacks resources to collect | Your case is not a priority for current IRS collection staff |

| Older balance due | The debt has been sitting unresolved for an extended time |

| No active resolution program | No installment agreement, OIC, or hardship status is currently active |

The IRS does not transfer every account. Certain taxpayers are protected from PDC referrals, including those in active bankruptcy, victims of identity theft, deceased taxpayers, minors, and individuals currently working with the Taxpayer Advocate Service.

Which Private Collection Agencies Does the IRS Use?

The IRS contracts with a small number of approved agencies. As of the most recent update, the authorized private collection agencies are:

- CBE Group (Cedar Falls, Iowa)

- Coast Professional Inc. (Albion, New York)

- ConServe (Fairport, New York)

- Performant Recovery (Livermore, California)

- Pioneer Credit Recovery (Arcade, New York)

The IRS updates its list of active contractors periodically. You can verify the current authorized agencies directly through the IRS Private Debt Collection program page. If anyone contacts you claiming to collect an IRS debt and is not on this list, do not pay them. Tax scams frequently mimic IRS collection activity.

How the CP40 Process Works: Step by Step

Understanding the sequence of events helps you respond correctly and avoid costly mistakes.

- Step 1: You receive the CP40 notice by mail. The IRS sends this first, before the collection agency contacts you. The notice includes the agency’s name and a Taxpayer Authentication Number you will need to verify the legitimacy of future contacts.

- Step 2: The assigned collection agency sends a letter. Within a few days of the IRS notice, the collection agency sends its own letter confirming the assignment. This letter must also include IRS contact information and your rights as a taxpayer.

- Step 3: The agency may call you. After the letters are sent, the agency is permitted to call. They must follow Fair Debt Collection Practices Act (FDCPA) rules. They cannot threaten, harass, or misrepresent the debt.

- Step 4: You respond, resolve, or request removal. You have options at this stage. You can set up a payment plan through the agency, pay in full, or, if you qualify, request that your account be removed from the PDC program entirely.

What Private Collectors Can and Cannot Do?

This is one of the most important sections to understand before you speak with anyone from a collection agency.

They CAN:

- Contact you by mail and phone during permitted hours

- Discuss your balance and payment options

- Set up direct debit installment agreements

- Accept payments made payable to the U.S. Treasury

They CANNOT:

- Accept payment made directly to the agency itself

- Threaten legal action, arrest, or deportation

- Demand unusual payment methods such as gift cards, wire transfers, or cryptocurrency

- Continue contacting you after you request a cease of communication in writing

- Negotiate Offers in Compromise or other complex resolution programs

- Override IRS decisions about your account

If anyone claiming to represent the IRS or a private collector asks for payment by gift card or wire transfer to a personal account, hang up. The IRS and its authorized partners do not collect that way.

Your Rights When the IRS Assigns Your Debt to a Collector?

Taxpayers retain full rights under both the Taxpayer Bill of Rights and the Fair Debt Collection Practices Act throughout the PDC process. The Consumer Financial Protection Bureau (CFPB) provides detailed guidance on your rights when dealing with any third-party debt collector, including those working under government contracts. Key protections include:

- The right to verify the debt before paying anything

- The right to request that collection cease while you dispute the amount

- The right to be removed from PDC if you are experiencing economic hardship

- The right to work directly with the IRS if you prefer

- The right to representation: you can authorize a licensed CPA or attorney to communicate on your behalf

Can You Stop the Private Collection Agency From Contacting You?

Yes, in several situations. You can request removal from the PDC program if you:

- Are in active bankruptcy

- Are currently working with the IRS on an installment agreement or other resolution

- Qualify as currently-not-collectible due to financial hardship

- Have a pending Offer in Compromise

- Have requested Innocent Spouse relief

- Are under active audit or in Tax Court proceedings

If you believe you should not have been referred, or if you want to move your account back to direct IRS management, contacting a qualified tax professional is the fastest path. A licensed CPA can file a Power of Attorney, communicate with both the IRS and the agency, and place your account in the appropriate resolution program.

What Happens If You Ignore a CP40 Notice??

Ignoring the notice does not make the debt go away. The IRS retains full ownership of your account even when a collection agency is managing it. Ignoring collection contacts can lead to:

- Escalation back to active IRS collections

- A federal tax lien filed against your property

- A levy on your bank account or wages

If you have received a CP40 and are unsure what to do, do not wait. The IRS continues accruing penalties and interest on the balance throughout the collection process. Our guide to federal tax lien help explains what can happen when an unresolved balance leads to a lien on your assets.

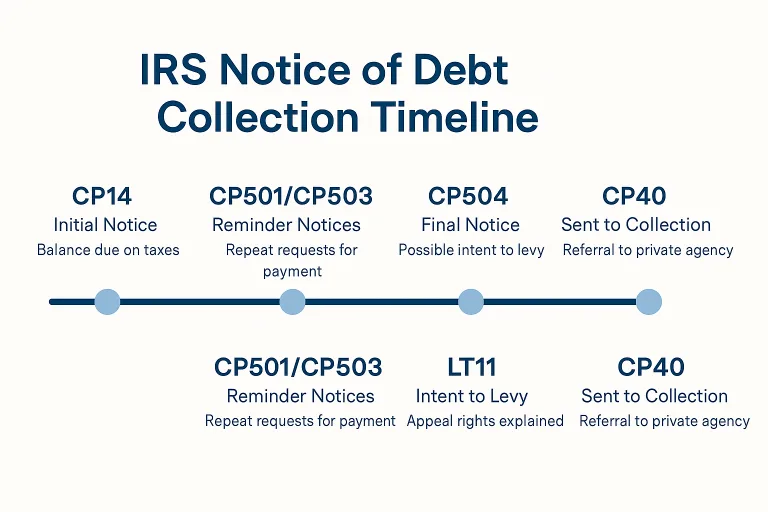

CP40 vs. Other IRS Collection Notices: How They Compare

Taxpayers often confuse the CP40 with other collection notices they may have received before it. Here is a quick comparison:

| Notice | What It Means | Urgency Level |

| CP14 | First notice of balance due | Low to Moderate |

| CP501 / CP503 | Reminder notices, balance still owed | Moderate |

| CP504 | Final notice before levy action | High |

| LT11 / Letter 1058 | Final Notice of Intent to Levy | Very High |

| CP40 | Account assigned to private collector | Moderate to High |

If you received a CP504 notice before the CP40, your account had already reached a critical enforcement stage. If an LT11 Final Notice of Intent to Levy was issued at any point, your Collection Due Process (CDP) hearing rights may have been triggered and the clock on those rights is running.

Should You Work With the Collection Agency or the IRS Directly?

Most taxpayers with a CP40 are better served by resolving through the IRS directly, particularly if the balance is large, involves multiple tax years, or includes penalties that may be abatable. The private collection agency can only offer limited payment arrangements. They cannot:

- Evaluate your eligibility for penalty abatement

- Negotiate a reduction in the total amount owed

- Submit an Offer in Compromise

- Place you in currently-not-collectible status

For straightforward balances where a full-pay installment agreement is feasible, working with the agency is reasonable. For anything more complex, engaging our IRS tax resolution services gives you access to the full range of resolution options rather than the narrow set the collection agency can offer.

Verifying the Contact Is Legitimate

Before providing any information or making any payment, confirm the following:

- You received a CP40 from the IRS in the mail first

- The agency contacting you matches the name on your CP40

- The agency is listed on the IRS authorized contractor page

- Any payment you make is directed to the U.S. Treasury, never to the agency itself

According to the IRS official CP40 guidance, the IRS will never initiate contact by phone without a prior written notice, and legitimate collectors will never demand immediate payment without allowing you time to verify the debt.

What to Do Right Now If You Received a CP40?

- Read the notice carefully and note the assigned agency name

- Do not make any payment before verifying the debt amount and your options

- Check whether you qualify for removal from the PDC program

- Consider whether penalty abatement or an installment agreement through the IRS directly makes more sense for your situation

- If the balance is large or you have other unresolved tax issues, consult a licensed CPA before responding

At Ed Parsons CPA, we review CP40 situations as part of a full account analysis. We pull your IRS transcripts, assess your resolution options, and communicate with the IRS on your behalf if removal from the PDC program is warranted.

Got a CP40 Notice? Do Not Pay Before You Read This.

Our CPA team reviews your full IRS account, identifies your best resolution path, and handles communication with the IRS and the collection agency on your behalf.

Schedule a Free Consultation with Ed Parsons CPA

Ed Parsons CPA specializes in IRS tax resolution, collections defense, and state tax representation for clients in Massachusetts, Florida, and nationwide.