Skip to content

Skip to content

The Cost of Skipping IRS Streamlined Procedures

The Cost of Skipping IRS Streamlined Procedures

Taxpayers who forgo IRS Streamlined Filing Compliance Procedures lose access to reduced penalty structures designed specifically for non-willful offshore noncompliance. Without that pathway, prior-year delinquent returns and unfiled FBARs face standard IRS enforcement, including substantial information-return penalties, potential fraud exposure. No formal mechanism for penalty mitigation.

Key Takeaways

Taxpayers who bypass streamlined procedures face full statutory IRS penalties on unreported foreign financial assets including FBAR penalties, failure-to-file penalties, and information return penalties with no procedural protection or penalty mitigation available. Qualifying expats under the foreign track pay 0% in miscellaneous offshore penalties; outside the program, FBAR penalties, failure-to-file penalties, and information return penalties stack across multiple years and accounts.

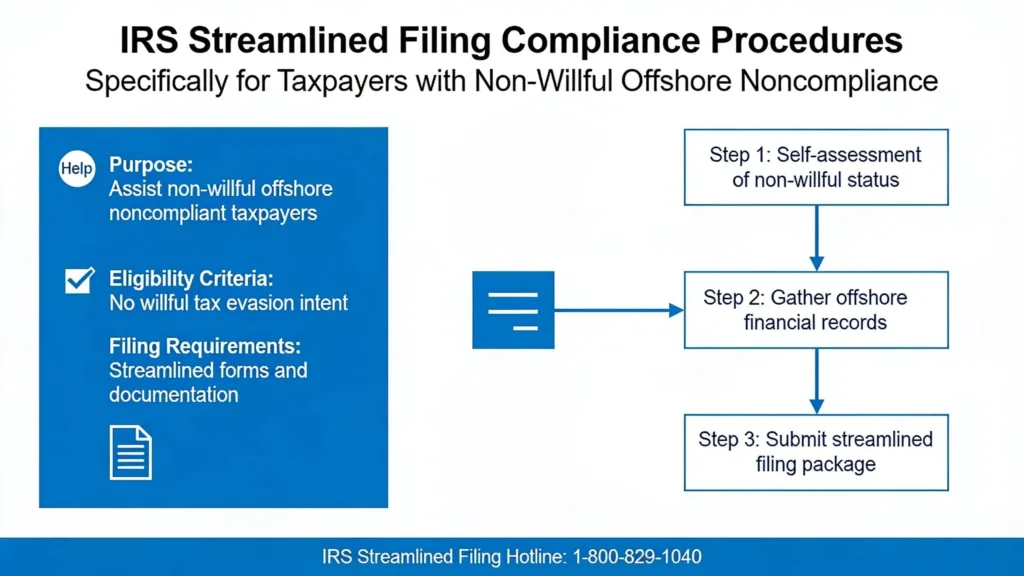

Non-willful non-compliance requires filing three years of tax returns and six years of FBARs.

Once the IRS initiates contact or opens an examination, streamlined eligibility closes making early action the only way to preserve access to reduced penalty terms.

Willful violations result in criminal prosecution, substantial fines, and potential imprisonment for tax evasion.

Taxpayers who bypass streamlined procedures face full statutory IRS penalties on unreported foreign financial assets including FBAR penalties, failure-to-file penalties, and information return penalties with no procedural protection or penalty mitigation available. Qualifying expats under the foreign track pay 0% in miscellaneous offshore penalties; outside the program, FBAR penalties, failure-to-file penalties, and information return penalties stack across multiple years and accounts.

Non-willful non-compliance requires filing three years of tax returns and six years of FBARs.

Once the IRS initiates contact or opens an examination, streamlined eligibility closes making early action the only way to preserve access to reduced penalty terms.

Willful violations result in criminal prosecution, substantial fines, and potential imprisonment for tax evasion.

What Happens When You Skip Streamlined Procedures?

Taxpayers who forego streamlined filing specifically the IRS Streamlined Filing Compliance Procedures forfeit access to reduced penalty terms designed specifically for non-willful offshore noncompliance. The cost of inaction is not simply a delayed filing. It is full exposure to the IRS enforcement machinery with no procedural protection in place.

Streamlined procedures exist to give qualifying taxpayers a structured path: file delinquent or amended returns, resolve outstanding tax obligations, and close the compliance gap under favorable terms. Taxpayers who do not use that path forfeit the reduced penalties, penalty-free catch-up status, and procedural protections the program provides.

What Enforcement Actions Can the IRS Take Against Taxpayers Who Don’t File?

The IRS collections process runs on its own timeline, indifferent to whether a taxpayer has decided to act. Notices arrive first, followed by federal tax liens, account levies, and. For taxpayers with serious delinquencies passport restrictions or revocation. Expats face the same sequence as domestic taxpayers, with additional complexity layered on top.

Can the IRS Find Unreported Foreign Accounts Without a Taxpayer’s Help?

The IRS does not need a taxpayer to self-report in order to identify unreported foreign accounts. Foreign financial institutions in more than 100 countries are legally required to report U.S. account holders to the IRS under FATCA (Foreign Account Tax Compliance Act) data-sharing agreements. That means accounts a taxpayer never disclosed are often already visible to the IRS before any voluntary action is taken.

The practical risk breakdown looks like this:

Penalty exposure: Full statutory penalties apply outside the streamlined framework

Enforcement escalation: Liens, levies, and passport action remain available to the IRS

Reduced negotiating position: Proactive disclosure carries more weight than a response to IRS contact

Penalty exposure: Full statutory penalties apply outside the streamlined framework

Enforcement escalation: Liens, levies, and passport action remain available to the IRS

Reduced negotiating position: Proactive disclosure carries more weight than a response to IRS contact

Waiting does not reduce the problem. It removes the options.

What Penalties Apply Outside the Streamlined Program?

Taxpayers who bypass the IRS Streamlined Procedures face a dramatically steeper penalty landscape than those who use the program. The gap between streamlined rates and standard IRS penalty rates is stark: a qualifying expat under the foreign track pays 0% in miscellaneous offshore penalties, while a taxpayer outside the program faces stacked FBAR penalties, failure-to-file penalties, and information return penalties that compound across multiple years and accounts.

The streamlined program offers two tracks with sharply different costs:

Track

Residency Requirement

Miscellaneous Offshore Penalty

IRS Streamlined Procedures: Typical Service Costs

At least 330 days outside the U.S. in one of the three most recent tax years

0%

Key Differences in IRS Streamlined Filing Options Explained

U.S.-based filers who do not meet the foreign residency test

5% of highest aggregate account balance

Outside these tracks, standard FBAR penalties, failure-to-file penalties, accuracy-related penalties, and information return penalties apply and they stack.

How Does the IRS Detect Unreported Foreign Accounts?

Detection risk is higher than many non-filers expect. The IRS uses FBAR cross-referencing, comparing FinCEN data from annual FinCEN Form 114 filings against tax returns to identify unreported foreign income. Taxpayers who have not filed are not invisible they are simply unresolved.

What Happens When a Taxpayer Waits Too Long?

Delay does more than narrow options it changes the nature of the conversation with the IRS entirely. Once an examination opens or the IRS contacts a taxpayer about a specific account or return, the streamlined path closes and the taxpayer shifts from a voluntary disclosure posture to a defensive one. At that point, the IRS controls the timeline, the scope of inquiry expands beyond what the taxpayer might have disclosed voluntarily, and penalty mitigation becomes a negotiation rather than a program benefit. Acting before that threshold is crossed is the only way to preserve the procedural advantages the streamlined program provides.

Ed Parsons CPA carries deep experience with Streamlined Filing Compliance Procedures and multi-year catch-up filings involving forms such as Form 2555, Form 1116, Form 5471, Form 8621, Form 8938, and FinCEN Form 114. Addressing the exposure now, while the streamlined path remains open, is the most defensible position available.

Who Qualifies for Streamlined Foreign Offshore Procedures?

Streamlined Foreign Offshore Procedures are available to individual U.S. taxpayers who meet a specific non-residency requirement and can certify that prior failures to report foreign financial assets resulted from non-willful conduct. Missing either condition disqualifies a taxpayer from the program entirely.

Qualification rests on two pillars:

Non-residency requirement – the taxpayer must satisfy the applicable physical presence or residency test for the relevant period; for joint filers, both spouses must independently meet this standard

Non-willful conduct – a non-willful FBAR violation is one where the failure to report foreign income and pay the related tax stemmed from oversight, misunderstanding, or lack of awareness, not intentional avoidance; a willful FBAR violation, by contrast, involves deliberate concealment and carries far harsher penalties

Non-residency requirement – the taxpayer must satisfy the applicable physical presence or residency test for the relevant period; for joint filers, both spouses must independently meet this standard

Non-willful conduct – a non-willful FBAR violation is one where the failure to report foreign income and pay the related tax stemmed from oversight, misunderstanding, or lack of awareness, not intentional avoidance; a willful FBAR violation, by contrast, involves deliberate concealment and carries far harsher penalties

What Filing Obligations Does the Program Require?

Qualifying taxpayers must file three years of delinquent federal tax returns. Specifically the most recent years for which the filing deadline has passed. Along with six years of FBARs (FinCEN Form 114). These filings must be complete and accurate. Partial submissions do not satisfy the program’s requirements.

What Is Form 14653 and Why Does It Matter?

Form 14653 is the certification statement taxpayers submit alongside their streamlined package. On this form, the taxpayer certifies under penalty of perjury that the prior non-compliance was not willful. The certification is not a formality. A weak or inconsistent narrative can undermine the entire submission. Critically, taxpayers must come forward before the IRS initiates contact once an examination or inquiry begins, the streamlined path closes.

The stakes of a flawed submission are significant. A certification later deemed insufficient can expose a taxpayer to the full penalty structure that the IRS Streamlined Procedures were designed to avoid.

Who Qualifies for Streamlined Domestic Offshore Procedures?

Streamlined Domestic Offshore Procedures apply to U.S. taxpayers who do not meet the non-residency requirement that governs the foreign version of the program. Taxpayers who have been living and working inside the United States and therefore cannot satisfy that physical presence test use the domestic path instead.

The distinction matters. The foreign version carries a 0% penalty for qualifying expats. The domestic version imposes a 5% miscellaneous offshore penalty on the highest aggregate balance of unreported foreign assets. Choosing the wrong track, or skipping the program entirely, exposes taxpayers to far steeper civil penalties and potential criminal referral.

What Happens With Joint Filers Under the Domestic Procedures?

Joint return filers face a specific rule. For a married couple filing jointly, the domestic procedures apply when one spouse, both spouses. Either spouse fails to meet the non-residency requirement. A couple where one partner lived abroad and the other remained stateside would typically fall under the domestic track, not the foreign one.

Who Should Review Eligibility Before Filing?

Eligibility is not always obvious. Residency determinations involve specific IRS criteria, and a misclassification. Filing under the foreign procedures when the domestic rules actually apply — can undermine the entire disclosure. Ed Parsons CPA has represented hundreds of taxpayers through offshore disclosure. International compliance matters, including more than 100 taxpayers in Offshore Voluntary Disclosure Initiative matters, along with extensive work on Streamlined and delinquent international filings. That depth of case experience allows for precise eligibility analysis before a single return is prepared.

The qualifying criteria are narrow. Getting them right at the outset protects the entire filing position.

When Should You Consult a CPA About Streamlined Filing?

The right time to consult a CPA about Streamlined Filing is the moment a taxpayer discovers any gap in foreign financial reporting not after an IRS notice arrives. Delayed action narrows the available compliance options and increases the risk of penalties that the IRS Streamlined Procedures are specifically designed to avoid.

Many clients reach Ed Parsons CPA after uncovering problems such as:

Unfiled FBARs (FinCEN Form 114) for foreign bank or investment accounts

Foreign corporation reporting requirements, including missed Form 5471 filings

PFIC complications tied to foreign mutual funds or pooled investments

Foreign brokerage accounts, cryptocurrency held abroad, or years of missed U.S. returns

IRS notices referencing international information returns

Unfiled FBARs (FinCEN Form 114) for foreign bank or investment accounts

Foreign corporation reporting requirements, including missed Form 5471 filings

PFIC complications tied to foreign mutual funds or pooled investments

Foreign brokerage accounts, cryptocurrency held abroad, or years of missed U.S. returns

IRS notices referencing international information returns

The pattern is consistent. A taxpayer realizes the filing gap, searches for answers. Then needs someone to reconstruct the full picture before any disclosure is made.

What Does a CPA Actually Do in a Streamlined Case?

Ed Parsons CPA organizes the underlying facts, reconstructs missing filing history, identifies every applicable reporting obligation. Prepares accurate returns and disclosures. The goal is a clear, defensible filing position not just paperwork submitted and forgotten.

Why Does Direct CPA Access Matter for These Cases?

Complex international compliance cases require fast, accurate issue spotting. Ed Parsons CPA handles these matters personally, without routing clients through layers of junior staff. That direct access produces clearer communication and reduces the risk that a critical detail. A foreign trust, a second account, a missed form gets overlooked during the intake and analysis process.

Frequently Asked Questions

What happens to penalty rates when you skip IRS Streamlined Procedures?

Full statutory penalties apply outside the streamlined framework. FBAR penalties alone can reach $10,000 per account per year for non-willful violations, and willful FBAR penalties can reach the greater of $100,000 or 50% of the account balance per violation. Failure-to-file penalties, accuracy-related penalties, and information return penalties stack on top of those figures across multiple years and accounts with no program-based mitigation available.

Does the IRS need you to self-report your foreign accounts to find them?

No. Under FATCA, foreign financial institutions in more than 100 countries are legally required to report U.S. account holders directly to the IRS. Accounts a taxpayer never disclosed are often already visible to the IRS before any voluntary action is taken. FBAR cross-referencing against FinCEN Form 114 data adds a second layer of detection risk.

What is a non-willful FBAR violation, and why does it matter for streamlined eligibility?

A non-willful FBAR violation is one where the failure to report foreign financial assets resulted from oversight, misunderstanding, or lack of awareness not deliberate concealment. Non-willful conduct is the threshold condition for streamlined eligibility. Willful violations are disqualifying and carry far steeper civil penalties and potential criminal referral.

What enforcement actions does the IRS take against taxpayers who don’t file?

The IRS collections process runs on its own timeline. Notices arrive first, followed by federal tax liens, account levies, and for taxpayers with serious delinquencies passport restrictions or revocation. Expats face the same enforcement sequence as domestic taxpayers, with additional complexity tied to international information return obligations.

When does the streamlined filing window close?

The streamlined path closes the moment the IRS initiates contact or opens an examination related to a taxpayer’s foreign accounts or returns. Once that threshold is crossed, the taxpayer moves from a voluntary disclosure posture to a defensive one, and penalty mitigation becomes a negotiation rather than a program benefit. Acting before IRS contact is the only way to preserve access to the program’s reduced penalty terms.

What is the difference between the Streamlined Foreign Offshore and Streamlined Domestic Offshore Procedures?

The foreign track applies to U.S. taxpayers who meet a specific non-residency requirement at least 330 days outside the U.S. in one of the three most recent tax years and carries a 0% miscellaneous offshore penalty. The domestic track applies to U.S.-based filers who do not meet that residency test and imposes a 5% miscellaneous offshore penalty on the highest aggregate balance of unreported foreign financial assets. Filing under the wrong track can undermine the entire disclosure.

Conclusion

The IRS Streamlined Filing Compliance Procedures exist for a specific reason: to give taxpayers with non-willful offshore noncompliance a structured, penalty-reduced path back into compliance before the IRS acts first. As this article has shown, the cost of skipping that path is not abstract it is the full weight of FBAR penalties, failure-to-file penalties, and information return penalties stacking across multiple years and accounts, with no procedural protection in place.

The window is not permanently open. Once the IRS initiates contact or opens an examination, the streamlined path closes and the taxpayer shifts from a voluntary posture to a defensive one. For U.S. expats and domestic taxpayers alike, the only way to preserve access to the program’s reduced penalty terms is to act before that threshold is crossed.

Taxpayers who have identified a gap in their foreign financial reporting unfiled FBARs, unreported foreign income, missed information returns should consult a CPA with deep experience in offshore disclosure before taking any filing action. The analysis of eligibility, residency classification, and willfulness certification must be done correctly at the outset. A flawed submission can be as damaging as no submission at all.

Ready to Resolve Your Offshore Filing Gap?

If you’ve identified unreported foreign accounts, unfiled FBARs, or missed international information returns, the time to act is now before the IRS does. Edward Parsons, CPA handles Streamlined Filing Compliance Procedures personally, without routing clients through junior staff.

Call us at [+1 (786) 265-8578](tel:+17862658578) or email [edwardweb@edparsonscpa.com](mailto:edwardweb@edparsonscpa.com) to schedule a consultation. You can also visit edparsonscpa.com to learn more about our offshore disclosure services.