Skip to content

Skip to content

When the Florida Department of Revenue uses the markup method, it estimates your restaurant’s sales from your purchases and treats any shortfall as unreported and taxable. That estimate rests on assumptions that are frequently wrong: the markup percentage, the sample period, and the reductions left out. A CPA reviews the audit by reconciling the auditor’s workpapers, testing the assumed markup against your real food cost and product mix, re-examining the sample for representativeness, and applying documented reductions the auditor ignored. The goal is a corrected, defensible number presented at the Notice of Intent to Make Audit Changes stage, before the assessment becomes final.

A Florida markup assessment can look intimidating and authoritative. Pages of schedules, projected sales, and a large balance due. What it rarely shows is how many assumptions are stacked inside that final number.

A markup calculation is an estimate built on choices the auditor made. Each choice can be tested, and many can be reduced. Here is how an experienced CPA takes that calculation apart.

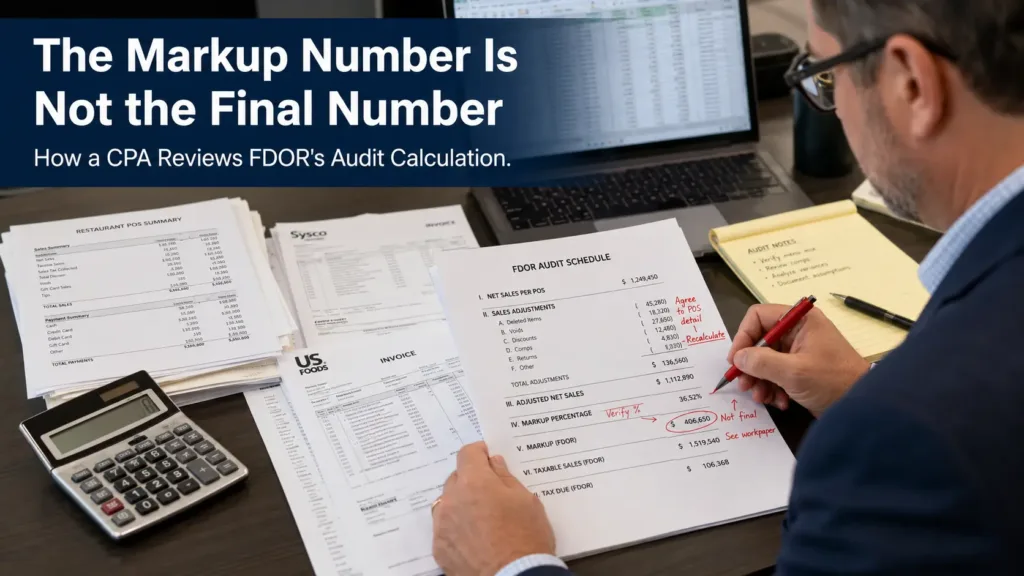

The Markup Number Is a Starting Point, Not a Verdict

The markup method multiplies your food and beverage cost by an assumed markup to produce expected sales. If your reported sales are lower, the gap is taxed across the audit period.

Because the math is leveraged, a small error in the assumed markup swings the assessment by tens of thousands of dollars. The full mechanics are covered in our guide to the Florida restaurant markup method. For defense purposes, the key point is that the number is negotiable until it is finalized.

Step One: Reconcile the Auditor’s Workpapers

The first task is to obtain and reconcile the auditor’s workpapers. A CPA traces exactly how the auditor arrived at the cost base, where the markup came from, which periods were sampled, and how the projection was built.

This step alone often surfaces errors: purchases double-counted, non-food items swept into the cost base, or a markup pulled from a generic benchmark that does not fit your concept. You cannot challenge what you have not reconstructed, and reconstructing the auditor’s math is where the defense begins.

Testing the Assumed Markup Against Reality

Next, the CPA tests the markup itself. The auditor’s percentage is compared against your actual food and beverage cost, your menu pricing, and your real product mix. A bar-heavy concept, a high-waste kitchen, and a quick-service counter all carry very different true markups.

How FDOR Builds the Number vs What a CPA Examines

| Audit Element | How FDOR Builds It | What a CPA Examines |

| Markup percentage | Often a generic industry benchmark | Your actual food cost, pricing, and product mix |

| Sample period | A few months projected across years | Whether the months reflect your real seasonality |

| Reductions | Frequently omitted | Spoilage, comps, employee meals, theft, documented |

| Sales classification | Treated broadly as taxable | Exempt grocery sales and gratuity coding separated out |

| Math and period | Accepted as calculated | Arithmetic, projection, and statute of limitations verified |

| Measurement (how the number is recomputed) | Expected sales = cost x assumed markup, gap taxed | Expected sales re-derived from verified cost and mix, documented reductions applied, and the error rate recomputed from a representative sample |

Re-Examining the Sample

Most markup assessments ride on a sample. A CPA tests whether the periods the auditor chose actually represent your operation, because a peak or anomalous month distorts the entire projection. Our explanation of how Florida audit sampling works shows why an unrepresentative sample can multiply a small error into a multi-year liability. Re-deriving the error rate from a sound sample is one of the most effective reductions available.

The Reductions FDOR Often Leaves Out

Auditors rarely volunteer the adjustments that lower your number. A thorough review documents and asserts them:

- Spoilage, waste, comps, employee meals, and theft that consume cost without producing taxable sales.

Exempt grocery and food-product sales that were swept in as taxable, the line explained in our guide to prepared food vs groceries.

Gratuities miscoded as taxable, covered in our article on tip and gratuity sales tax.

- Use tax already paid, or items not actually subject to tax, removed from the base.

The DR-1215 Window: When to Respond

Florida issues preliminary findings on a Notice of Intent to Make Audit Changes, Form DR-1215. This is the critical moment. Responding here, with reconciled workpapers, a corrected markup, a sound sample, and documented reductions, is far more effective than disputing a finalized assessment later.

Once findings are final, your path narrows to formal protest and appeal. Acting at the DR-1215 stage is the difference between a working negotiation and an uphill fight. A Business CPA Tax Resolution Case Analysis is built to do exactly this work on your numbers.

Common Mistakes Owners Make Before Calling a CPA

- Accepting the markup percentage as fixed rather than testing it.

- Signing off on a sample without checking whether the months are representative.

- Volunteering records that expand the cost base and the projection.

- Letting the DR-1215 window pass without a documented response.

- Trying to negotiate the balance without first correcting the underlying calculation.

How Ed Parsons, CPA Approaches a Florida Restaurant Audit?

With more than 25 years of tax resolution experience, Ed Parsons, CPA represents Florida restaurants through every stage of an FDOR sales tax audit, from the first DR-840 notice through the DR-1215 findings and any protest. The approach is methodical: control what the auditor sees, reconstruct the calculation, document every legitimate reduction, and present a corrected number the Department can accept.

The work begins with a Business CPA Tax Resolution Case Analysis, a focused review of your notice, your records, and the auditor’s math that identifies where the assessment is overstated and maps the response.

Frequently Asked Questions

Only what is appropriate, organized and framed correctly. Volunteering extra records can expand the cost base and the projection against you.

Talk to a CPA about your Florida audit

If FDOR has assessed your restaurant or a DR-1215 is in hand, the calculation can likely be reduced, but the window is short. Start with a Business CPA Tax Resolution Case Analysis, or speak with Ed Parsons, CPA directly.

visit our contact page to discuss your situation.