Skip to content

Skip to content

Florida use tax is the companion to sales tax. When a restaurant buys equipment, supplies, or decor from an out-of-state or online vendor that does not charge Florida tax, the business owes 6 percent use tax, plus any county surtax, directly to the state. Under section 212.06, Florida Statutes, the duty to pay shifts to the buyer when the seller does not collect. Because these purchases sit quietly in your fixed asset and depreciation records, auditors treat use tax as low-hanging fruit. A single large kitchen equipment purchase made without tax can produce thousands of dollars on one audit line.

Most restaurant owners know they collect sales tax on meals. Far fewer realize they may owe tax on what they buy. That second obligation is use tax, and it is one of the easiest adjustments for a Florida auditor to make, because it is often a clean, documented number sitting in your own records.

What Use Tax Actually Is

Sales tax applies when a Florida seller collects it at the register. Use tax applies when a taxable item is used in Florida but no Florida tax was collected at purchase, most often from an out-of-state or online vendor. When the seller does not charge it, the obligation moves to you as the buyer.

The rate matches sales tax: 6 percent state, plus any county surtax. If an out-of-state seller charged some tax but less than Florida’s rate, you generally owe only the difference.

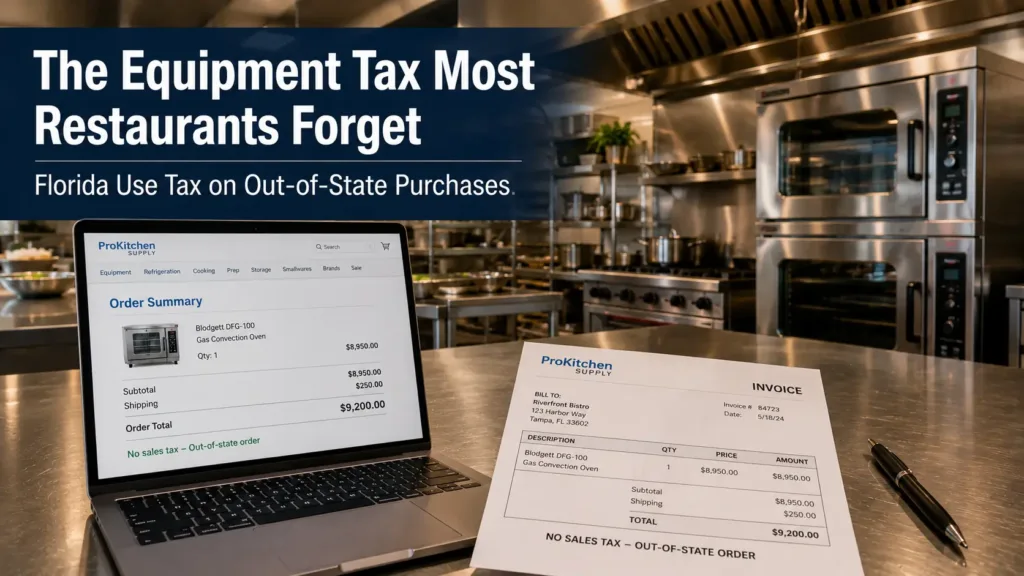

Why Restaurants Trigger It Without Realizing

Opening or remodeling a restaurant means buying equipment quickly, much of it from out-of-state suppliers and online marketplaces that do not collect Florida tax. Owners assume that if no tax appeared on the invoice, none was due. The opposite is true.

Because these are capital purchases, they land on your fixed asset and depreciation records, where they stay visible for years. That permanence is what makes them such a reliable audit target.

Taxed at Purchase vs Use Tax Owed

| Attribute | In-State Purchase (Florida tax collected) | Out-of-State / Online (no Florida tax) |

| At purchase | Seller charges Florida tax | No Florida tax, or less than 6 percent |

| Who owes the tax | Seller, at the register | The buyer, directly to the state |

| Florida result | Obligation satisfied | Use tax due (full 6 percent, or the shortfall) |

| Reporting | Nothing further required | Use tax line of your DR-15 |

| Measurement (how the auditor quantifies it) | Confirms tax on invoices | Ties fixed asset and depreciation schedules to invoices and bank payments, then assesses 6 percent plus surtax on untaxed purchases across the look-back period |

The standard Florida audit look-back is three years, so one missed year is rarely the whole exposure.

Where Auditors Find It

Use tax is attractive because the evidence is already organized, often by you:

- Fixed asset and depreciation schedules listing capital purchases by date and amount.

- Federal returns, where depreciation deductions point to equipment buys.

- Vendor invoices showing whether Florida tax was charged.

- Bank and card statements confirming payments to out-of-state sellers.

Purchases Most Often Missed

- Kitchen equipment ordered online or from out-of-state suppliers.

- Furniture, fixtures, and decor for the dining room or build-out.

- Smallwares, paper goods, and to-go packaging bought in bulk.

- Point-of-sale hardware, screens, signage, and out-of-state marketing materials.

- Leased or financed equipment, where the tax treatment is easy to get wrong.

Quick Facts Worth Knowing

- Use tax rate equals the sales tax rate: 6 percent plus any county surtax.

- If an out-of-state seller charged under 6 percent, you generally owe only the difference.

- Use tax is reported on the use tax line of your DR-15 return.

- Capital purchases stay on depreciation schedules for years, making them easy to audit.

- One large untaxed equipment purchase can drive a four-figure or larger adjustment.

Common Mistakes Restaurants Make

- Assuming no tax is due because the invoice showed none.

- Treating online and out-of-state equipment as tax-free.

- Never using the use tax line on the DR-15.

- Overlooking leased equipment and bulk supplies from out-of-state distributors.

- Leaving it unaddressed until the auditor finds it on the fixed asset schedule.

Questions Owners Actually Ask

I bought my ovens online and never saw a tax line, do I owe something? What about furniture shipped in from another state? Does leased equipment count? Those are the right questions, and they point to the exact purchases an auditor looks for.

Identifying which purchases created a use tax liability, and quantifying it before the Department does, is the work that happens inside a Business CPA Tax Resolution Case Analysis, where your fixed asset schedule, invoices, and returns are reviewed together rather than under audit pressure.

What to Do Before the Auditor Adds It Up

Use tax exposure is usually quantifiable in advance, which is why it should not wait for an audit. Knowing your number first changes your options, including whether a proactive disclosure beats reacting to an assessment.

Start with what a Florida DR-840 audit notice means and what happens next. If you suspect you already owe, the Florida Voluntary Disclosure Program may let you come forward on better terms than waiting for the audit. A Business CPA Tax Resolution Case Analysis estimates your realistic exposure and maps the cleanest way to address it.

Frequently Asked Questions

Next step

Bought equipment or supplies from out-of-state or online vendors? Find your use tax exposure before an auditor does. A Business CPA Tax Resolution Case Analysis reviews your fixed asset records and invoices and estimates the exposure.