Skip to content

Skip to content

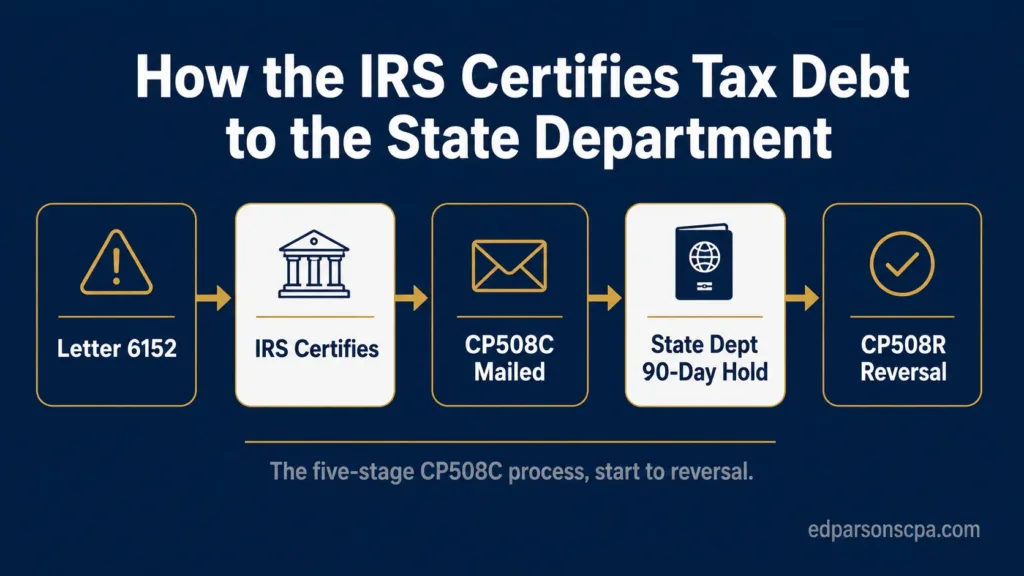

The CP508C process runs in five stages: the IRS flags a seriously delinquent balance and certifies it, the certification is transmitted to the State Department on a weekly cycle, the IRS mails Notice CP508C to the taxpayer, the State Department holds passport applications for 90 days, and once a qualifying resolution is recorded, the IRS issues CP508R to decertify, usually within 30 days. Each stage has its own timing, and missing the window at any step narrows the options at the next.

Most taxpayers meet the CP508C process only when something has already gone wrong: a denied renewal, a held application, or a notice they were not expecting. Understanding the procedural flow makes the difference between reacting late and acting in the right window.

This walkthrough follows the certification from the warning notice through final decertification, with the timing that applies at each stage.

Before CP508C: The Warning Notices

Certification is never the first step. The IRS works through its normal collection sequence first, including the balance due notice, reminder notices, the CP504 notice, and the Final Notice of Intent to Levy (LT11 or Letter 1058).

Closer to certification, the IRS issues Letter 6152, the Notice of Intent to Request the State Department Revoke Your Passport. Under IRS procedures, this letter goes out at least 30 days before a revocation referral, or 90 days if it is mailed to an address outside the United States.

The Five-Stage CP508C Process

Stage 1: The IRS Certifies the Debt

When the balance meets all five statutory conditions, the IRS systemically posts a certification transaction code to the account. The certification is then transmitted to the U.S. State Department on a weekly cycle, not on the day of the decision.

The five conditions that must be satisfied are the same ones detailed in the CP508C notice overview.

Stage 2: CP508C Is Mailed to the Taxpayer

At the same time the certification is transmitted, the IRS mails Notice CP508C by regular mail to the taxpayer’s last known address. It is not sent electronically and not copied to a power of attorney.

This is why some taxpayers, especially those who have moved, never see the notice and learn of certification only when a passport action occurs.

Stage 3: The State Department Acts

Once the State Department holds a certification, it can deny a new application, refuse a renewal, revoke an existing passport, or issue a limited-validity passport for direct return to the United States.

If you apply for or renew a passport after certification, the State Department generally holds the application open for 90 days from the date of its letter, giving you time to resolve the debt or correct an erroneous certification.

Stage 4: A Qualifying Resolution Is Recorded

Decertification does not happen because you start working on the problem. It happens when the IRS records a specific qualifying resolution on the account. Paying below the threshold alone does not reverse certification.

Stage 5: CP508R Reverses the Certification

When the account meets a reversal condition, the IRS reverses the certification code and notifies the State Department. The taxpayer receives Notice CP508R, the reversal of certification, generally within 30 days of the qualifying resolution.

Because each certified tax year stands on its own, full decertification requires every certified module to be reversed. The detailed reversal conditions are published in the IRS Passport Program manual, IRM 5.19.25.

The Certification Timeline at a Glance

The table below maps each stage to its typical timing.

| Stage | What Happens | Typical Timing |

| Pre-certification warning | IRS issues Letter 6152, Notice of Intent to Request Revocation | At least 30 days before referral (90 days if mailed abroad) |

| Certification | IRS posts a certification code to the account and transmits it to the State Department | Transmitted on a weekly cycle |

| CP508C issued | IRS mails CP508C to the last known address (not copied to power of attorney) | Same time as certification |

| State Department action | Holds new applications, may revoke, deny, or limit a passport | 90-day hold from the State Department letter date |

| Reversal (CP508R) | IRS reverses certification after a qualifying resolution and notifies the State Department | Up to 30 days after resolution recorded |

| Measurement | Each certified tax module stands on its own; decertification requires the last module to be reversed | Per IRM 5.19.25 procedures |

The Resolution Paths That Trigger Reversal

Certification reverses only when one of these qualifying conditions is recorded:

- Full payment of the seriously delinquent balance

- An accepted installment agreement being paid on time

- An accepted Offer in Compromise

- Currently Not Collectible status due to hardship

- A pending innocent spouse relief request

- A timely requested or pending CDP hearing on the relevant levy

- A determination that the certification was erroneous

Most of these paths require a financial disclosure on Form 433-F, the Collection Information Statement, which is where the resolution begins to take shape.

Common Mistakes in the Certification Process

- Treating Letter 6152 as junk mail instead of the final warning it is

- Assuming certification happens the same day the IRS decides (it transmits weekly)

- Believing the State Department can reverse certification (only the IRS can)

- Paying below the threshold and expecting automatic reversal

- Missing that each certified tax year must be individually reversed

- Letting the 90-day State Department window lapse without a recorded resolution

Questions Taxpayers Actually Ask

“How long does it take the IRS to certify after Letter 6152?”

Letter 6152 goes out at least 30 days before a referral, or 90 days if mailed abroad. Certification then transmits to the State Department on a weekly cycle.

“Will CP508C and CP508R arrive on the same timeline?”

No. CP508C is mailed when certification occurs. CP508R is issued after a qualifying resolution, usually within 30 days of that resolution being recorded.

“If I set up an installment agreement, when does my passport free up?”

Once the agreement is accepted and recorded, the IRS reverses certification and notifies the State Department, generally within 30 days.

“Does each tax year get its own certification?”

Effectively yes. Each certified module stands on its own, and decertification requires the last certified module to be reversed.

Where the Process Gets Complicated?

The flow looks linear on paper. In practice, verifying which modules were certified, confirming the qualifying resolution was recorded correctly, and timing the CP508R against an upcoming trip all require reading the account the way the IRS reads it.

A Personal CPA Tax Resolution Case Analysis pulls the IRS account transcripts, confirms exactly which tax periods were certified, verifies the transaction codes behind the certification, and identifies the fastest qualifying path to CP508R for your specific situation.

For the underlying record review, see how IRS account transcripts reveal the certification codes, and for the statutory basis, see what Section 7345 actually says. The IRS publishes the program rules on its passport revocation page.

.")