Skip to content

Skip to content

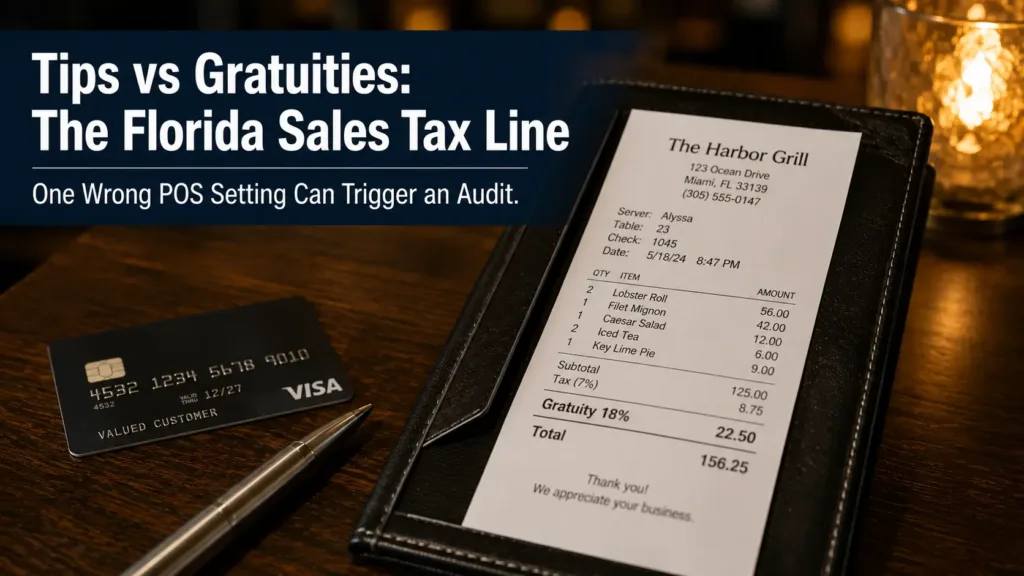

In Florida, a voluntary tip a customer chooses to leave is not subject to sales tax, but a mandatory or automatic gratuity the restaurant adds to the bill generally is, because it becomes part of the taxable sales price. Under Florida Administrative Code Rule 12A-1.0115(7)(a), an added gratuity is excluded from tax only when it is separately stated on the receipt and the restaurant keeps no part of it. If any portion stays with the business, even to cover a credit card fee, the charge can become fully taxable. Restaurants that lump tips and mandatory gratuities together in their point-of-sale system create exactly the gap auditors look for.

Tips feel like the simplest part of running a restaurant. A guest leaves a little extra, it goes to the server, and that is the end of it. For sales tax, it is not that simple.

Florida draws a sharp line between a tip a customer chooses to leave and a gratuity the restaurant requires. Get the line wrong, and a routine audit can reclassify thousands of dollars of gratuities as taxable sales. Here is how the rule actually works and where restaurants lose.

The Core Rule: Optional Versus Mandatory

The deciding factor is who controls the charge. If the customer decides whether to leave the gratuity and how much, it is voluntary. If the restaurant adds it automatically, it is mandatory.

Florida treats the two very differently:

- A voluntary tip is the customer’s own decision and is not part of the price the restaurant charges, so it is not subject to sales tax.

- A mandatory or automatic gratuity is a charge the restaurant imposes, so it becomes part of the taxable sales price and is generally taxed like the meal itself.

This is the part many owners, and even some bookkeepers, get backward. The automatic 18 to 20 percent added to a large party is not a tip in the tax sense. It is a charge by the business.

When a Mandatory Gratuity Is Still Exempt

There is an exception, and it is narrow. Under Florida Administrative Code Rule 12A-1.0115(7)(a), an added gratuity can be excluded from the taxable sales price only when two conditions are both met:

- It is separately stated as a gratuity, tip, or similar charge on the customer’s receipt.

- The restaurant receives no monetary benefit from it, meaning the full amount goes to employees.

Both conditions matter. If a mandatory gratuity is buried in the total instead of broken out, or if the restaurant keeps any slice of it, the exception does not apply and the charge is taxable. A binding Florida Technical Assistance Advisement reached this same conclusion: a separately stated gratuity passed entirely to employees stayed exempt precisely because the restaurant kept none of it.

Routine payroll handling of the employee’s own share of taxes does not, by itself, count as the restaurant benefiting. But keeping a portion to offset costs, including credit card processing fees on the gratuity, can push the entire charge into taxable territory. The details decide the outcome, and the details are where exposure hides.

Voluntary Tip vs Mandatory Gratuity: How Florida Treats Each

| Attribute | Voluntary / Optional Tip | Mandatory / Automatic Gratuity |

| Who sets the amount | The customer chooses to leave it | The restaurant adds it to the bill |

| Part of the sales price? | No, it is the customer’s decision | Yes, it is a charge by the business |

| Florida sales tax treatment | Generally not taxable | Generally taxable as part of the meal |

| Key exception | Already exempt | Exempt only if separately stated AND 100% goes to employees |

| Common audit trigger | Mislabeling a required charge as a voluntary tip | Lumped with tips in the POS, or restaurant keeps a portion |

| Measurement (how the auditor quantifies it) | Reconciles reported tips to POS detail and payroll records | Compares federal gross receipts and reported gratuities against sales tax returns, then taxes the unreconciled difference |

Florida’s combined rate is the 6 percent state sales tax plus any county discretionary surtax, so the exposure on reclassified gratuities scales with your location.

How a Florida Auditor Spots Gratuity Problems

Auditors rarely take your sales tax returns at face value. They cross-check them against other numbers you have already reported.

The most common move is a reconciliation. If your federal income tax return shows gross receipts or tip income that is larger than the taxable sales on your DR-15 returns, the auditor treats the difference as potentially unreported taxable sales. Unless you can prove those amounts were genuinely voluntary tips passed entirely to employees, the gap gets taxed.

Your point-of-sale system is the other weak point. When auto-gratuity and voluntary tips share the same line or category, the auditor cannot tell them apart, and neither can you after the fact. That ambiguity almost always resolves in the Department’s favor.

Other Charges That Get Taxed Like Gratuities

The gratuity rule extends to several charges restaurants do not think of as tips at all. These are generally taxable because they are amounts the business requires:

- Service charges and automatic large-party charges.

- Minimum charges, such as a per-person food and beverage minimum.

- Corkage and setup fees.

- Cover charges, including admission for live music or events.

Each of these can quietly add to a gratuity assessment if it was not taxed correctly at the point of sale.

Quick Facts Worth Knowing

- Voluntary tip = not taxable. Mandatory gratuity = taxable, unless separately stated and fully paid to employees.

- Keeping even a small portion of a mandatory gratuity, including to cover card fees, can make the whole charge taxable.

- Auditors reconcile federal gratuity and gross receipt figures against state DR-15 returns and tax the difference.

- A POS that does not separate tips from auto-gratuities is one of the most common restaurant audit findings.

- The exposure runs at 6 percent plus your county surtax, multiplied across the full audit period.

Common Mistakes Restaurants Make

- Treating an automatic large-party gratuity as a non-taxable tip.

- Coding voluntary tips and mandatory gratuities to the same POS field.

- Retaining part of a mandatory gratuity to offset credit card fees, then assuming it stays exempt.

- Failing to separately state the gratuity on the customer receipt.

- Leaving federal and state figures unreconciled, so the gap looks like unreported taxable sales.

- Not taxing service charges, minimums, corkage, setup, and cover charges that follow the same rule.

Questions Restaurant Owners Actually Ask

If you are wondering things like: Do I charge sales tax on the automatic 18 percent for a party of eight? What if I keep a little of the service charge for the kitchen? Why is the auditor looking at my federal return for a sales tax audit? You are asking the right questions, and they are exactly the ones that separate a clean audit from a costly one.

Sorting your real exposure on gratuities, service charges, and POS coding before an auditor does is the kind of review that happens inside a Business CPA Tax Resolution Case Analysis, where your receipts, returns, and federal numbers are examined together rather than line by line under audit pressure.

What to Do Before an Audit Looks at Your Gratuities

The fix is rarely complicated once it is identified, but identifying it correctly requires looking at your receipts, your POS configuration, your payroll flow, and your federal returns at the same time. That is hard to do under the time pressure of an active audit and easy to do beforehand.

If you add automatic gratuities or service charges, the safest step is a focused review of how they are stated, coded, and distributed. A Business CPA Tax Resolution Case Analysis maps your gratuity exposure and shows where the Department is most likely to push, before a notice ever arrives.

For the broader picture, start with what a Florida DR-840 audit notice means and what happens next, and see how the line between prepared food and groceries creates the same kind of POS classification risk.

Frequently Asked Questions

Next step

If your restaurant adds automatic gratuities or service charges, review how they are stated, coded, and distributed before an auditor does. A Business CPA Tax Resolution Case Analysis maps your gratuity exposure and shows where the Department is most likely to push.