Skip to content

Skip to content

IRS Streamlined Filing: Options for Delinquent Returns

IRS Streamlined Filing: Options for Delinquent Returns

By Edward Parsons

The IRS Streamlined Procedures offer a penalty-reduced path for non-willful delinquent filers, requiring 3 years of returns and 6 years of FBARs. Alternatives like the Voluntary Disclosure Program suit willful violations but carry steeper penalties. Edward Parsons, CPA in Doral, FL helps clients determine the correct program for their situation.

Key Takeaways

The IRS Streamlined Procedures require taxpayers to certify their delinquent filings were the result of non-willful conduct not deliberate concealment.

Streamlined Foreign Offshore Procedures (SFOP) carry no miscellaneous offshore penalty; Streamlined Domestic Offshore Procedures (SDOP) impose a 5% penalty on the highest aggregate unreported foreign account balance.

A complete Streamlined submission covers 3 years of back tax returns and 6 years of FinCEN Form 114 (FBAR) filings.

Willful violations disqualify taxpayers from all Streamlined tracks; the IRS Voluntary Disclosure Program (VDP) applies instead but carries significantly higher penalties.

For joint filers, both spouses must independently satisfy the non-residency requirement to use the Streamlined Foreign Offshore Procedures.

An active IRS examination or DOJ investigation disqualifies a taxpayer from using Streamlined Procedures acting promptly after discovering a delinquency is critical.

Correct program selection between SFOP, SDOP, Delinquent FBAR Submission Procedures, and VDP is one of the most consequential decisions in any offshore compliance matter.

The IRS Streamlined Procedures require taxpayers to certify their delinquent filings were the result of non-willful conduct not deliberate concealment.

Streamlined Foreign Offshore Procedures (SFOP) carry no miscellaneous offshore penalty; Streamlined Domestic Offshore Procedures (SDOP) impose a 5% penalty on the highest aggregate unreported foreign account balance.

A complete Streamlined submission covers 3 years of back tax returns and 6 years of FinCEN Form 114 (FBAR) filings.

Willful violations disqualify taxpayers from all Streamlined tracks; the IRS Voluntary Disclosure Program (VDP) applies instead but carries significantly higher penalties.

For joint filers, both spouses must independently satisfy the non-residency requirement to use the Streamlined Foreign Offshore Procedures.

An active IRS examination or DOJ investigation disqualifies a taxpayer from using Streamlined Procedures acting promptly after discovering a delinquency is critical.

Correct program selection between SFOP, SDOP, Delinquent FBAR Submission Procedures, and VDP is one of the most consequential decisions in any offshore compliance matter.

What Are IRS Streamlined Procedures for Delinquent Filings?

IRS Streamlined Procedures are a formal compliance framework for U.S. taxpayers with unreported foreign financial assets. First introduced in 2012 and since expanded, the program has one core requirement: the taxpayer’s failure to report must not have resulted from willful conduct. Taxpayers who meet that standard gain access to a structured path toward compliance with significantly lower penalties than a standard IRS enforcement action.

Who Qualifies for the Streamlined Procedures?

Eligibility hinges on the non-willfulness standard. Taxpayers must certify that missed filings and unreported income stemmed from oversight, misunderstanding, or lack of awareness not deliberate concealment. Two tracks exist based on residency:

Streamlined Foreign Offshore Procedures (SFOP) for taxpayers residing outside the United States

Streamlined Domestic Offshore Procedures (SDOP) for U.S.-resident taxpayers

Streamlined Foreign Offshore Procedures (SFOP) for taxpayers residing outside the United States

Streamlined Domestic Offshore Procedures (SDOP) for U.S.-resident taxpayers

What Tax Problems Do the Streamlined Procedures Resolve?

The procedures address three categories of delinquency: unreported income from foreign financial assets, unfiled FBAR (FinCEN Form 114) filings, and FATCA reporting gaps under Form 8938. FBAR penalties alone can reach $10,000 per account per year for non-willful violations; willful FBAR penalties can reach the greater of $100,000 or 50% of the account balance per violation. FATCA failures carry a separate $10,000 penalty per unfiled return, with additional penalties up to $50,000 for continued non-compliance.

A single foreign account can trigger FBAR, FATCA, and corporate information return requirements simultaneously. Identifying every applicable obligation before filing is what separates a defensible submission from one that creates new exposure.

Ed Parsons CPA has represented hundreds of taxpayers through offshore disclosure and international compliance matters, including extensive work with Streamlined filings across both tracks.

Who Qualifies: Domestic vs. Foreign Streamlined Procedures?

IRS Streamlined Procedures divide into two tracks based on residency. Taxpayers who cannot satisfy the non-residency requirement use the domestic track; those who can access the foreign track, which carries no miscellaneous offshore penalty.

Qualification Factor

Streamlined Domestic (SDOP)

Streamlined Foreign (SFOP)

Residency

U.S.-based taxpayer

Must meet non-residency requirement

Joint filers

One spouse qualifies

Both spouses must meet non-residency requirement

Conduct standard

Non-willful

Non-willful

Penalty structure

5% miscellaneous offshore penalty

No miscellaneous offshore penalty

Both tracks share the same threshold: the failure to report income from a foreign financial asset must have resulted from non-willful conduct. Willful failures disqualify a taxpayer from either streamlined path.

What does “non-willful” mean for streamlined eligibility?

Non-willful conduct means the failure arose from negligence, inadvertence, or a misunderstanding of U.S. reporting obligations not a deliberate decision to hide assets. The IRS evaluates the full facts and circumstances. A taxpayer who simply did not know about FBAR or FATCA requirements is a fundamentally different case from one who actively concealed accounts or provided false information to a financial institution.

What happens when joint filers have different residency situations?

Both spouses must independently satisfy the non-residency requirement to use the foreign track. If one spouse does not qualify, the couple cannot use the foreign procedures and must use the domestic track, absorbing the 5% penalty.

Ed Parsons CPA works with expatriates, dual citizens, and U.S. taxpayers holding foreign accounts to assess which streamlined track fits their specific facts before any filing is prepared.

How Does Streamlined Compare to Other Delinquent Filing Options?

Four primary programs exist for taxpayers with offshore reporting gaps:

Streamlined Foreign Offshore Procedures (SFOP) for qualifying non-residents; no miscellaneous offshore penalty

Streamlined Domestic Offshore Procedures (SDOP) for U.S.-resident taxpayers; 5% miscellaneous offshore penalty on the highest aggregate balance

Delinquent FBAR Submission Procedures (DFSP) for taxpayers who missed FinCEN Form 114 filings but have no unreported income

Delinquent International Information Return Submission Procedures (DIIRSP) for taxpayers with unfiled international information returns (Forms 5471 or 8621) but no associated tax liability

Streamlined Foreign Offshore Procedures (SFOP) for qualifying non-residents; no miscellaneous offshore penalty

Streamlined Domestic Offshore Procedures (SDOP) for U.S.-resident taxpayers; 5% miscellaneous offshore penalty on the highest aggregate balance

Delinquent FBAR Submission Procedures (DFSP) for taxpayers who missed FinCEN Form 114 filings but have no unreported income

Delinquent International Information Return Submission Procedures (DIIRSP) for taxpayers with unfiled international information returns (Forms 5471 or 8621) but no associated tax liability

Each program targets a different fact pattern. Selecting the wrong one creates a filing position the IRS can challenge.

What Happens When Conduct May Be Willful?

Taxpayers whose offshore failures rise to willful conduct are not eligible for Streamlined programs. The IRS Voluntary Disclosure Program (VDP) is the separate pathway for those situations. VDP carries higher penalties, a formal multi-step process, and a longer resolution timeline. In serious cases, willful FBAR failures can also carry criminal exposure making the willful versus non-willful determination one of the most consequential decisions in any offshore compliance matter.

How Does a CPA Determine Which Program Applies?

Program selection depends on residency status, the nature and value of unreported assets, whether tax was owed, years of delinquency, and an honest assessment of the taxpayer’s state of mind. A taxpayer with a missed FBAR and no unreported income may qualify for Delinquent FBAR Submission Procedures, avoiding a miscellaneous offshore penalty entirely. A taxpayer with unreported foreign income and deliberate account structuring faces a different set of options and potentially the Voluntary Disclosure Program or worse.

Ed Parsons CPA organizes the underlying facts, reconstructs missing filing history, identifies all applicable reporting obligations, and prepares returns and disclosures that support a clear and defensible filing position.

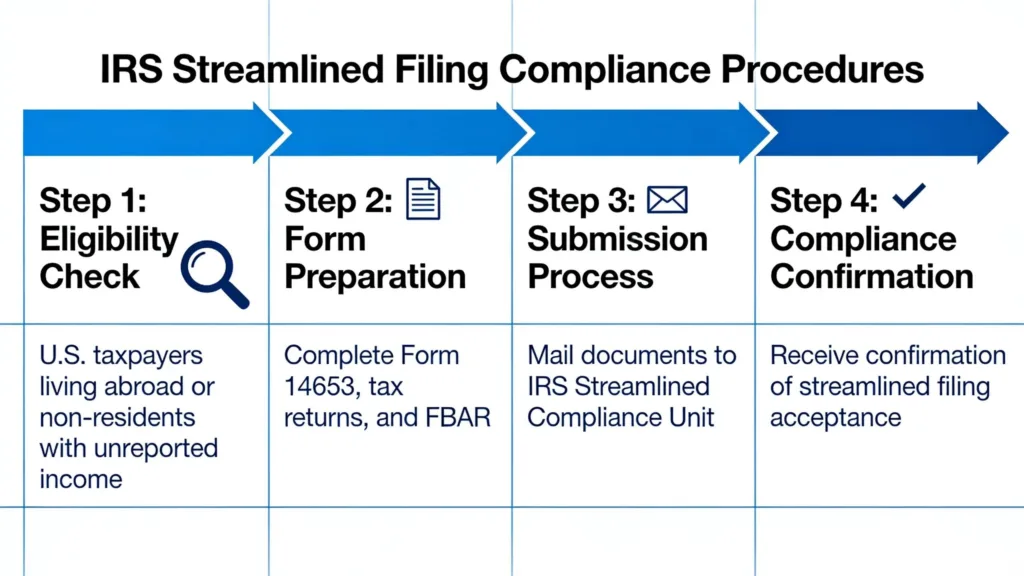

What Forms and Years Does a Streamlined Submission Require?

A Streamlined submission covers 3 years of amended or delinquent income tax returns and 6 years of FinCEN Form 114 (FBAR) filings. Common forms required include:

Form 2555 – Foreign Earned Income Exclusion

Form 1116 – Foreign Tax Credit

Form 5471 – Information Return for Foreign Corporations

Form 8621 – PFIC (Passive Foreign Investment Company) reporting

Form 8938 – FATCA Statement of Specified Foreign Financial Assets

FinCEN Form 114 – FBAR, filed separately through the BSA E-Filing System

Form 2555 – Foreign Earned Income Exclusion

Form 1116 – Foreign Tax Credit

Form 5471 – Information Return for Foreign Corporations

Form 8621 – PFIC (Passive Foreign Investment Company) reporting

Form 8938 – FATCA Statement of Specified Foreign Financial Assets

FinCEN Form 114 – FBAR, filed separately through the BSA E-Filing System

Missing even one form changes the entire compliance posture. A single unfiled Form 5471 carries a $10,000 penalty per year per entity, and Form 8621 omissions can affect the tax treatment of the underlying investment.

What happens when a taxpayer filed some years but missed others?

Partial filing history creates a layered compliance problem. The Streamlined procedures are specifically designed to let taxpayers reconstruct a defensible filing history across the required period including FBARs for years where returns were filed but the FBAR was not.

Why do clients discover these obligations late?

Many clients reach Ed Parsons CPA after uncovering unfiled FBARs, foreign corporation reporting requirements, or years of missed U.S. returns often triggered by a bank inquiry, a FATCA notice, or a conversation with a foreign financial institution. Acting quickly after discovery is what keeps the most favorable options open. Delays can allow an IRS examination to begin, which disqualifies a taxpayer from Streamlined procedures entirely.

Why Does Working With a CPA Matter for Streamlined Filings?

Working with a qualified CPA directly affects whether a Streamlined submission succeeds or creates new exposure. The Eligibility for IRS Streamlined Filing Options certification carries legal weight that a poorly prepared filing cannot recover from.

What Makes the Non-Willfulness Certification So Consequential?

The non-willfulness certification is a signed statement the IRS scrutinizes. A vague or inconsistent narrative gives the IRS grounds to reject the submission or to treat it as an admission of willfulness, converting a manageable compliance matter into a potential criminal referral. A credible narrative must explain how the taxpayer first learned about the account, why reporting obligations were missed, and what steps were taken upon discovering the oversight. Getting those facts organized and presented consistently across every submitted form is the foundation on which the entire submission rests.

How Does Direct CPA Access Change the Outcome?

Ed Parsons CPA works directly with clients not through layers of junior staff to identify reporting obligations, reconstruct prior-year filings, prepare accurate disclosures, and build a defensible strategy. Ed has represented hundreds of taxpayers in Streamlined and offshore disclosure matters, meaning the patterns, pitfalls, and documentation standards are already familiar.

Accurate non-willfulness narrative construction

Prior-year filing reconstruction

Identification of all applicable reporting obligations

Defensible, consistent filing position across all submitted years

Accurate non-willfulness narrative construction

Prior-year filing reconstruction

Identification of all applicable reporting obligations

Defensible, consistent filing position across all submitted years

FAQ

What is the key requirement to qualify for IRS Streamlined Procedures?

Taxpayers must certify that their delinquent filings resulted from non-willful conduct meaning oversight, misunderstanding, or lack of awareness, not deliberate concealment. The certification must be supported by a credible, fact-specific narrative. A vague or poorly documented certification can give the IRS grounds to reject the submission or reclassify the conduct as willful, significantly increasing penalty exposure.

How do the Streamlined Foreign and Domestic Offshore Procedures differ?

The Streamlined Foreign Offshore Procedures (SFOP) apply to U.S. taxpayers residing outside the United States and carry no miscellaneous offshore penalty. The Streamlined Domestic Offshore Procedures (SDOP) serve U.S.-resident taxpayers and impose a 5% miscellaneous offshore penalty on the highest aggregate balance of unreported foreign financial assets over the covered period. For joint filers, SFOP requires both spouses to independently satisfy the non-residency requirement.

What happens if a taxpayer’s conduct was willful?

Willful violations disqualify taxpayers from Streamlined Procedures entirely. The IRS Voluntary Disclosure Program (VDP) is the separate pathway, but it carries substantially higher penalties, a multi-step process, and a longer resolution timeline. In the most serious cases, willful FBAR failures can also carry criminal exposure making an accurate willfulness assessment before any filing is submitted essential.

How many years of returns and FBARs does a Streamlined submission require?

A Streamlined submission covers 3 years of amended or delinquent income tax returns and 6 years of FinCEN Form 114 (FBAR) filings. The specific international information returns required such as Forms 5471, 8621, or 8938 depend on the taxpayer’s individual foreign financial profile and must be identified before the submission is prepared.

Can a taxpayer use Streamlined Procedures if an IRS examination is already underway?

No. If the IRS has opened an examination covering any of the years included in the Streamlined submission, the taxpayer is generally disqualified. The same applies if the IRS or Department of Justice has initiated a civil or criminal investigation. Acting quickly after discovering a delinquency is critical delays can close off the most favorable compliance options entirely.

What penalties apply under each Streamlined track compared to willful FBAR violations?

Under SFOP, there is no miscellaneous offshore penalty eligible non-residents pay only the tax owed plus interest. Under SDOP, a 5% miscellaneous offshore penalty applies. By contrast, non-willful FBAR penalties can reach $10,000 per account per year outside a streamlined program, while willful FBAR penalties can reach the greater of $100,000 or 50% of the account balance per violation.

How long does the Streamlined filing process typically take?

A straightforward submission with organized records and a single foreign account can often be prepared within several weeks. Cases involving multiple foreign entities, PFIC investments, or years of missing records can take several months to reconstruct accurately. Acting promptly after discovery is what preserves the option to use Streamlined Procedures at all.

Ready to Resolve Your Delinquent Filing Exposure?

If you’ve discovered unfiled FBARs, unreported foreign accounts, or missed international information returns, acting quickly is what keeps the most favorable options open. Edward Parsons, CPA works directly with taxpayers expats, dual citizens, and domestic residents with foreign accounts to assess eligibility, prepare defensible Streamlined submissions, and navigate the full range of IRS compliance programs.

Contact Ed Parsons CPA today to discuss your situation:

ð +1 (786) 265-8578

ð edparsonscpa.com

ð 11601 Lakeside Dr, Doral, FL 33178

ð +1 (786) 265-8578

ð edparsonscpa.com

ð 11601 Lakeside Dr, Doral, FL 33178