Skip to content

Skip to content

FBAR vs Form 8938: Key Differences in Foreign Account Reporting

FBAR vs Form 8938: Key Differences in Foreign Account Reporting Explained

By Edward Parsons, CPA, Edward Parsons, CPA

Navigating the complexities of foreign account reporting can be daunting for U.S. taxpayers. Specifically, two essential forms—FBAR (Foreign Bank and Financial Accounts Report) and Form 8938 (Statement of Specified Foreign Financial Assets)—serve distinct purposes but can create confusion among those required to file them. This article provides a comprehensive comparison of FBAR and Form 8938, clarifying their unique requirements, filing processes, and penalties for non-compliance. Many individuals struggle with the nuances of these forms, which can lead to costly penalties. Understanding the key differences ensures that taxpayers stay compliant with their reporting obligations. We will explore the purpose of each form, the thresholds for filing, the associated penalties, and how these forms may overlap in reporting requirements.

Purpose

FBAR and Form 8938 serve as crucial compliance tools for U.S. taxpayers with foreign financial interests. FBAR focuses specifically on U.S. persons declaring foreign bank accounts, while Form 8938 encompasses a broader spectrum of foreign assets, including securities and certain foreign trusts. The legislative basis for FBAR comes from the Bank Secrecy Act, aiming to combat tax evasion, while Form 8938 is part of the Foreign Account Tax Compliance Act (FATCA), designed to ensure that U.S. taxpayers report specific foreign financial assets.

Filing Thresholds

Understanding the filing thresholds for FBAR and Form 8938 is critical for compliance. FBAR mandates filing when the aggregate value of foreign financial accounts exceeds $10,000 at any point during the calendar year. In contrast, Form 8938 has higher thresholds based on the taxpayer’s filing status and residency. For single U.S. residents, the threshold is $50,000 in foreign assets at year-end or $75,000 at any time during the year. Married taxpayers filing jointly have a $100,000 threshold at year-end or $150,000 at any point in the year.

Filing Process

The filing processes for FBAR and Form 8938 differ significantly. FBAR must be submitted electronically via the Financial Crimes Enforcement Network (FinCEN) website, and it is not part of the taxpayer’s annual tax return. Conversely, Form 8938 is submitted along with the taxpayer’s annual return and is filed directly with the IRS. This fundamental difference emphasizes the importance of knowing which forms must be filed in conjunction with each other to ensure compliance.

Penalties for Non-Compliance

Failing to comply with FBAR and Form 8938 filing requirements can result in severe penalties. FBAR violations can lead to civil penalties of up to $10,000 for non-willful violations and substantially higher fines for willful violations, potentially reaching up to $100,000 or 50% of the account balance. On the other hand, Form 8938 penalties can include an initial penalty of $10,000, with additional fines escalating for each month of non-compliance, and potentially even criminal penalties for willful disregard of reporting requirements. Taxpayers must acknowledge these risks to prevent hefty fines and other legal repercussions.

Overlap

FBAR and Form 8938 overlap in their filing requirements, which can confuse many taxpayers. Both forms may involve similar foreign financial accounts, meaning that one taxpayer might be required to file both forms for the same account. However, filing one form does not exempt individuals from needing to file the other if thresholds are met. Understanding this overlap is crucial for avoiding potential penalties and ensuring compliance.

What Are FBAR Filing Requirements for U.S. Taxpayers?

U.S. persons—including citizens, residents, and entities—must file an FBAR if they have a financial interest in or signature authority over foreign financial accounts exceeding the $10,000 threshold at any point in the calendar year. This includes all types of foreign accounts, such as savings accounts, checking accounts, and mutual funds. Ensuring that all applicable accounts are reported is critical to mitigate the risk of penalties.

Who Must File FBAR and What Are the Foreign Account Thresholds?

Eligibility for FBAR filing hinges on specific account balances and types. U.S. persons with cumulative balances across all foreign financial accounts exceeding $10,000 during the year must file. It is essential to consider all accounts where the taxpayer has a financial interest or signature authority, as cumulative values across multiple accounts can trigger the filing requirement.

Which Foreign Financial Assets Must Be Reported on FBAR?

The FBAR reporting requirements encompass a variety of foreign financial assets, primarily focusing on foreign bank accounts. Required assets include checking and savings accounts held at foreign banks, securities accounts, and even certain types of foreign mutual funds. Additionally, accounts where the individual holds signature authority but no financial interest must also be declared on the FBAR.

How Do Form 8938 Reporting Thresholds and Requirements Differ?

The thresholds for Form 8938 reporting are notably higher than those for FBAR, highlighting the distinct roles these forms play in U.S. tax compliance. Form 8938 requires reporting for specified foreign financial assets that exceed $50,000 for individuals or $100,000 for joint filers at year-end. The scope encompasses a broader range of financial assets, including foreign stocks, securities, non-U.S. pension plans, and foreign real estate.

What Specified Foreign Financial Assets Require Form 8938 Reporting?

Form 8938 requires the reporting of numerous specified foreign financial assets, which include foreign stocks, bank accounts, and partnerships. Taxpayers must provide descriptive information about these assets, including account numbers and the maximum value during the year. This detail is essential for accurate reporting and compliance with IRS regulations.

How Do Filing Thresholds Vary by Tax Filing Status and Residency?

Filing thresholds for Form 8938 vary significantly based on the taxpayer’s filing status and residency. For single filers residing in the U.S., the threshold stands at $50,000, while married couples filing jointly have a much higher threshold of $100,000. Non-resident taxpayers must also take into account different reporting limits, emphasizing the importance of understanding one’s specific filing circumstances.

What Are the Key Differences Between FBAR and Form 8938 Reporting?

The distinctions between FBAR and Form 8938 reporting are vital for taxpayers to grasp. While FBAR focuses specifically on foreign bank accounts and requires filing when the threshold exceeds $10,000, Form 8938 encompasses a wider array of foreign financial assets with higher reporting thresholds. Furthermore, FBAR is filed separately with FinCEN, while Form 8938 is filed with the IRS as part of the annual tax return.

How Do FBAR and FATCA Compliance Overlap and Diverge?

FBAR and FATCA compliance intertwine as both are designed to increase transparency regarding U.S. taxpayers holding foreign accounts. While they share similar objectives, they diverge in their requirements; FBAR primarily concentrates on account balances, whereas FATCA emphasizes the reporting of all specified foreign financial assets. Therefore, it is important to ensure comprehensive compliance with both regulations.

What Are the Different Penalties for Noncompliance With Each Form?

The penalties for failing to comply with FBAR and Form 8938 can be severe, encompassing both civil and criminal violations. FBAR penalties can be particularly harsh, with significant fines for willful violations. Form 8938 penalties, while less severe, can still escalate quickly for ongoing non-compliance. Taxpayers must acknowledge these risks to prevent hefty fines and other legal repercussions. Noncompliance can lead to IRS actions such as levies and seizure of assets.

What Are the IRS Penalties and Risks for Foreign Account Reporting Noncompliance?

The risks associated with foreign account reporting non-compliance extend beyond financial penalties. Taxpayers may face increased scrutiny from the IRS, potentially leading to audits and investigations. Additionally, failing to report foreign accounts can result in loss of assets and increased legal complexity, making it essential for taxpayers to understand their obligations thoroughly.

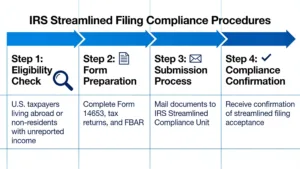

How Can Taxpayers Mitigate Penalties Using Streamlined Filing Procedures?

Taxpayers who realize they are non-compliant may still seek to rectify their situation through streamlined filing procedures. The IRS offers options to those who proactively address their filing lapses, often reducing penalties significantly while simplifying the disclosure process. Utilizing these procedures can be an effective method for minimizing negative implications of past mistakes.

How Does Professional Judgment Impact Complex Foreign Account Reporting?

Navigating the intricacies of foreign account reporting often requires the professional judgment of qualified tax advisors. These specialists can provide guidance on compliance strategies, ensuring taxpayers meet their filing obligations without incurring unnecessary penalties. Their insights are invaluable for those with complicated financial situations or international assets.

Why Is Professional Assistance Recommended for Delinquent Foreign Filings?

Receiving professional assistance with delinquent foreign filings can save taxpayers from significant mistakes. Given the complexities of FBAR and Form 8938, engaging a tax professional helps avoid the pitfalls of misunderstanding the requirements. This expertise can be particularly crucial for taxpayers who have substantial foreign holdings or complex financial structures.

What Are the Steps to Resolve International Filing Issues With IRS?

Resolving international filing issues with the IRS involves several key steps. Taxpayers should first gather all relevant documentation regarding their foreign accounts and financial assets. Next, they should consult with a tax professional to formulate an effective plan for addressing any discrepancies or unfiled returns. Finally, initiating contact with the IRS to discuss the situation transparently is crucial for mitigating penalties. Understanding IRS notices like the CP504 is vital during this process.

What Are the Practical Steps to Comply With FBAR and Form 8938 Requirements?

To ensure compliance with FBAR and Form 8938, taxpayers should follow several practical steps. These include:

- Documentation: Collect and organize all relevant financial statements and records for foreign accounts.

- Threshold Monitoring: Regularly assess account balances to determine filing obligations based on thresholds.

- Timely Filing: Submit required forms by the deadlines to avoid penalties.

By adhering to these steps, taxpayers can uphold their compliance responsibilities effectively.

What Are FBAR Reporting Requirements for U.S. Citizens?

FBAR requirements stipulate that U.S. citizens must file if they have financial interests in foreign accounts exceeding $10,000 during the year. This requirement applies to any combination of accounts that meet the threshold, necessitating a comprehensive understanding of eligibility and reporting obligations. A federal tax lien is a serious matter that can arise from unpaid taxes, underscoring the importance of timely and accurate reporting.

What Are Form 8938 Reporting Requirements for U.S. Citizens?

U.S. citizens must meet specific reporting requirements under Form 8938, including declaring specified foreign financial assets that exceed the designated thresholds based on filing status. Understanding these requirements helps ensure taxpayers remain compliant with their obligations regarding foreign assets.

How to Determine Filing Requirements Based on Foreign Asset Types?

Filing requirements can differ based on the types of foreign assets held. Taxpayers must evaluate the nature of their accounts, whether they are banks, stocks, or other financial interests, to determine the appropriate forms to file. This assessment is vital for ensuring accurate reporting and compliance with IRS regulations.

What Are the Filing Deadlines and How to Prepare Required Documentation?

Filing deadlines for FBAR and Form 8938 are critical for maintaining compliance. The FBAR must be filed electronically by April 15th, with an automatic extension to October 15th available. For Form 8938, the filing is due concurrently with the annual tax return. Preparing and organizing necessary documentation, such as account statements and ownership records, can help streamline the filing process and avoid errors.