Skip to content

Skip to content

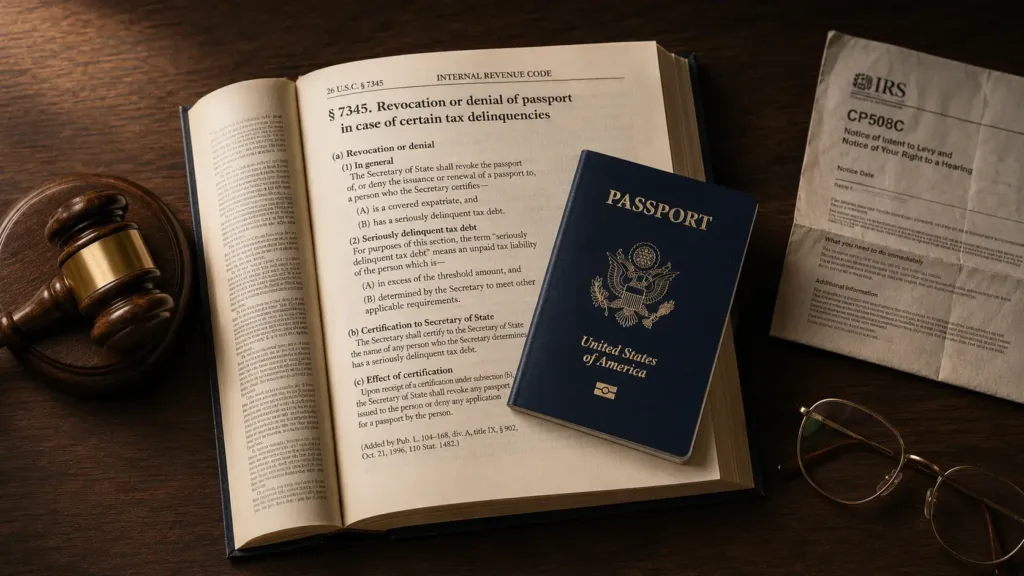

Yes, the federal government can revoke your U.S. passport for seriously delinquent tax debt. The mechanism is IRC Section 7345, enacted under the FAST Act of 2015 and in active use since 2018. Technically the IRS does not revoke passports; it certifies the debt to the State Department, which then has the authority to deny, refuse, revoke, or limit a passport. Federal courts have upheld the statute in every published constitutional challenge.

The short answer is yes, but the legal mechanics are more precise than most articles suggest. The IRS does not revoke passports directly. It certifies your tax debt as “seriously delinquent” under IRC Section 7345 and transmits that certification to the U.S. State Department, which holds the actual authority to act.

That distinction is why every constitutional challenge to the program has failed in federal court. This article walks through the statute, the leading cases, and what taxpayers most often misunderstand.

Where Section 7345 Came From?

Section 7345 was added to the Internal Revenue Code by the Fixing America’s Surface Transportation Act (FAST Act), signed into law in December 2015. Section 32101 of the same FAST Act gives the State Department the operational authority to act on IRS certifications.

The IRS began actively certifying taxpayers in early 2018. Hundreds of thousands of taxpayers have qualified for certification since the program launched.

What the Statute Authorizes the IRS to Do?

Section 7345 authorizes the IRS to do exactly two things:

- Determine that a taxpayer has “seriously delinquent tax debt” as defined in the statute

- Certify that determination to the Secretary of the Treasury, who must transmit it to the Secretary of State

The statute does not authorize the IRS to revoke a passport, hold one at the airport, or instruct the State Department to take any specific action. The actual passport authority comes from a different statute entirely.

How the IRS-to-State Department Chain Works?

The certification chain has three steps:

- Step 1: IRS determines the debt meets all five Section 7345 conditions and certifies it

- Step 2: IRS sends Notice CP508C to the taxpayer’s last known address

- Step 3: The State Department, acting under Section 32101 of the FAST Act, decides whether to deny, refuse, revoke, or limit the passport

For the full breakdown of what arrives in your mail when Step 2 happens, see CP508C notice can lead to passport revocation or denial. For the dollar threshold question,and seriously delinquent tax debt threshold and how it triggers passport action.

Court History: Why Every Challenge Has Failed

Three leading cases settled the major constitutional questions early in the program’s life.

| Case | Court / Year | Argument Raised | Holding |

| Maehr v. United States | 10th Circuit (2021), affirming D. Colo. (2020) | Section 7345 violates the constitutional right to international travel | Right to international travel is not fundamental; statute survives rational basis review |

| Rowen v. Commissioner | U.S. Tax Court, 156 T.C. No. 8 (2021) | Section 7345 violates Fifth Amendment Due Process and the UN Universal Declaration of Human Rights | Statute does not itself prohibit travel; revocation power sits with the State Department, not the IRS |

| Pfirrman v. Commissioner | U.S. Tax Court, T.C. Memo. 2025-22 | Certification was erroneous because the underlying assessment was disputed | Certification upheld; IRS only needed to show the five statutory elements were satisfied |

| Measurement | Reported decisions interpreting Section 7345 | Constitutional, due process, and statutory challenges | Every published challenge to date has been rejected |

The pattern across all three is consistent. Section 7345 itself does not restrict travel; it only authorizes the IRS to share information with the State Department. Passport action sits with the State Department under a separate statute, and the right to international travel is not a fundamental right that triggers strict scrutiny.

Why Constitutional Challenges Keep Losing?

- Section 7345 does not directly prohibit travel; courts read it as a notification mechanism

- International travel is treated as a liberty interest, not a fundamental right

- Under rational basis review, tax collection is a legitimate government interest

- Passport actions are taken by the State Department, not the IRS

- Due process arguments founder because Section 7345(e) provides a statutory remedy

What the IRS Cannot Do Under Section 7345?

- Revoke a passport directly (that authority belongs to the State Department)

- Certify debts below the inflation-adjusted threshold

- Certify debts being paid through an active installment agreement, accepted OIC, or CNC status

- Certify debts where appeal rights on the underlying lien are still open

- Bypass the requirement of a Notice of Federal Tax Lien filing or a levy issuance

Common Mistakes About Section 7345

- Believing the IRS itself revokes passports (it certifies; the State Department revokes)

- Assuming a constitutional challenge has a realistic chance of succeeding

- Confusing Section 7345 with general IRS collection authority

- Filing a challenge in the wrong forum or on the wrong grounds

- Fighting certification rather than resolving the underlying debt through a qualifying path

- Missing that pulling current IRS account transcripts is the first practical step

Questions Taxpayers Actually Ask

“Can the IRS really take my passport, or is this an exaggeration?”

The IRS triggers the action; the State Department executes it. Both pieces are real, both active since 2018, and federal courts have upheld the program.

“Is Section 7345 unconstitutional?”

Every published constitutional challenge has been rejected. Courts uphold the statute under rational basis review.

“Can I sue the IRS to stop a certification?”

You can petition the Tax Court under Section 7345(e), but only on grounds that the certification was erroneous. Constitutional arguments have not succeeded.

“Does it matter that the FAST Act is a transportation law?”

No. Courts have treated the substantive authority as fully valid.

What to Do If Your Passport Is at Risk?

Section 7345 is settled law. Challenging the statute itself is not a realistic strategy. The only practical path is to verify the certification, identify any erroneous elements, and resolve the underlying debt through one of the qualifying paths.

A Personal CPA Tax Resolution Case Analysis confirms whether the five statutory elements are satisfied, identifies any defect, and maps the fastest qualifying resolution path. That is the remedy the Maehr, Rowen, and Pfirrman courts all pointed to.

For prerequisite filings, see IRS tax lien help and the role of IRS account transcripts. The IRS publishes program rules on its passport revocation page, and the statute itself is available on Cornell Law’s Section 7345 page.