Skip to content

Skip to content

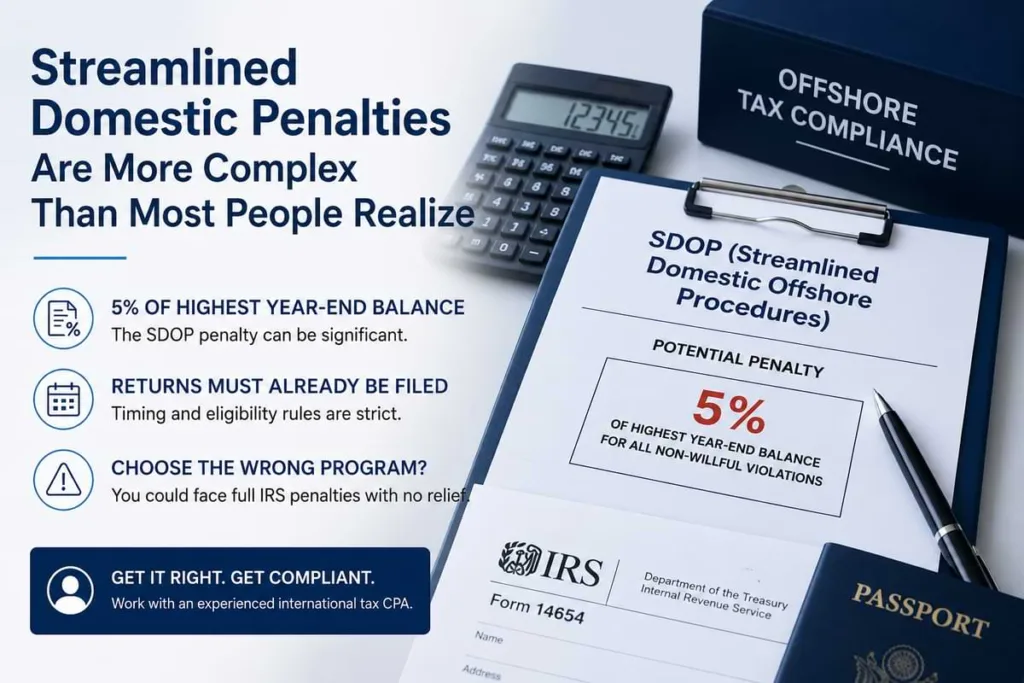

The 5% Streamlined Domestic Offshore Procedures (SDOP) penalty is calculated on the highest aggregate year-end value of all unreported foreign financial assets across the six covered years. The base includes far more than bank accounts. Foreign pensions, life insurance with cash value, foreign mutual funds, foreign corporation stock, and even foreign real estate held through an entity can all increase the penalty base. The highest year-end total across all six years drives the calculation, not the current balance.

Aisha estimated her streamlined penalty by multiplying her current foreign savings balance by 5%. Her account held about $80,000. Her math: $4,000.

The actual penalty was $12,300. She did not know her foreign pension counted. Or her cash-value life insurance. Or that the IRS uses the highest year-end balance across six years, not the current balance.

Most taxpayers underestimate the 5% SDOP penalty because they apply the percentage to the wrong base. The 5% rate is simple. What gets included in the base, and which year drives the calculation, is where the complexity lives.

What the 5% SDOP Penalty Actually Covers?

The Title 26 miscellaneous offshore penalty under SDOP is a fixed 5% applied to a single number: the highest aggregate year-end value of all unreported foreign financial assets across the covered years.

That definition contains three moving parts that determine the final penalty:

- What counts as a foreign financial asset

- Whether the asset was properly reported on the required form

- Which year-end value across the six covered years is the highest

Getting any one of these wrong changes the penalty calculation, sometimes by tens of thousands of dollars. Unlike the standard penalty framework for missed FBAR filings or Form 8938 violations, the SDOP penalty is not assessed per form or per year. It is a single aggregate calculation that captures everything missed.

What Is Included in the Penalty Base?

The SDOP penalty base includes any foreign financial asset that should have been reported but was not. The list is broader than most taxpayers expect.

| Measurement | Counted in the 5% Base | Excluded From the Base |

| Foreign bank accounts | Yes (if not reported on FBAR) | No (if properly reported) |

| Foreign mutual funds (PFICs) | Yes (if Form 8621 missing) | No (if properly reported) |

| Foreign pension/retirement | Yes, if Form 8938 obligation missed | Some treaty-protected accounts |

| Foreign insurance (cash value) | Yes (if unreported) | Term-only policies |

| Foreign corporation stock | Yes, if held directly and unreported | Held in a U.S. brokerage account |

| Foreign real estate (direct) | No | Always excluded if held directly |

| Foreign real estate via entity | Yes (interest in entity is included) | The real estate itself is not |

| Personal property abroad | No | Always excluded |

Foreign real estate held directly is one of the few clear exclusions. The moment that property is held through an entity, however, the situation reverses. An interest in a foreign corporation, partnership, or trust that owns real estate is itself a foreign financial asset and enters the penalty base.

Year-End Value vs Highest Balance: A Critical Distinction

This is one of the most misunderstood elements of the SDOP calculation. For FBAR purposes, the IRS uses the highest balance during the calendar year. For the SDOP penalty calculation, the IRS uses the year-end value.

This distinction creates several practical effects:

- A mid-year spike that did not exist at year-end is not in the SDOP base

- A pension or investment that grew significantly by December 31 sets a higher base

- Currency fluctuations matter because year-end exchange rates apply

- Selling an asset before year-end may eliminate it from that year’s calculation

The PFIC excess distribution calculation follows a different valuation logic again, which is why combined cases involving multiple unreported foreign positions require careful coordination across each calculation method.

How the Highest Aggregate Year-End Balance Is Calculated?

The SDOP calculation looks at six tax years: the three years covered by the streamlined amended returns plus the additional three years covered by the FBAR submission portion.

For each of those six years, the calculation involves:

- Identifying every unreported foreign financial asset held at year-end

- Converting each balance to U.S. dollars using year-end Treasury exchange rates

- Summing every asset value to arrive at that year’s aggregate

- Comparing the six aggregate figures and selecting the highest

The 5% penalty is then applied to that single highest aggregate figure. Not to each year. Not to each asset. One calculation, derived from the worst year in the look-back period.

A Worked Example: Why the Number Surprises People?

Aisha’s scenario across three of the six covered years, focusing only on three of her unreported assets:

| Year | Bank Account | Pension | Insurance | Year-End Total |

| Year 1 | $72,000 | $160,000 | $14,000 | $246,000 |

| Year 2 | $78,000 | $140,000 | $15,000 | $233,000 |

| Year 3 | $80,000 | $120,000 | $15,000 | $215,000 |

| Highest year-end aggregate | $246,000 (from Year 1) | |||

| 5% SDOP Penalty | $12,300 |

Year 1 produced the highest aggregate year-end balance at $246,000, driven by the higher pension valuation that year. The 5% penalty applied to that figure produced $12,300, regardless of what the balances looked like in Years 2 and 3. Aisha’s original estimate based only on her current bank balance missed the pension entirely and used the wrong year.

Common Mistakes in SDOP Penalty Calculations

- Using current account balances instead of historical year-end balances across all six covered years

- Excluding foreign pensions and retirement accounts that were never reported on Form 8938

- Treating foreign life insurance with cash value as a personal asset rather than a financial asset

- Forgetting foreign trust interests under Form 3520 or ownership obligations under Form 3520-A, both of which can add substantial value to the base

- Using FBAR-style highest-during-year balances instead of year-end values

- Applying spot exchange rates instead of year-end Treasury rates

- Reducing the base for assets that were properly reported only after the IRS contact, which does not count as timely reporting

The SDOP penalty calculation is one of the most technical components of any streamlined submission. A miscalculation either undercounts the penalty, which the IRS catches and rejects, or overcounts it, which costs the taxpayer money that was never owed. The Streamlined Filing CPA Package at Ed Parsons CPA covers the full penalty base review, the year-by-year valuation analysis, and the Form 14654 preparation with the non-willful narrative the IRS requires.