Skip to content

Skip to content

A rejected streamlined filing eliminates the 5% penalty reduction permanently for the assets covered in the submission. There is no formal appeal process, the IRS retains every document submitted, and the standard penalty structure applies in full. Total exposure after rejection typically increases by five to ten times the streamlined penalty. Voluntary Disclosure or reasonable cause abatement are the only remaining options, both significantly more difficult than the original streamlined path.

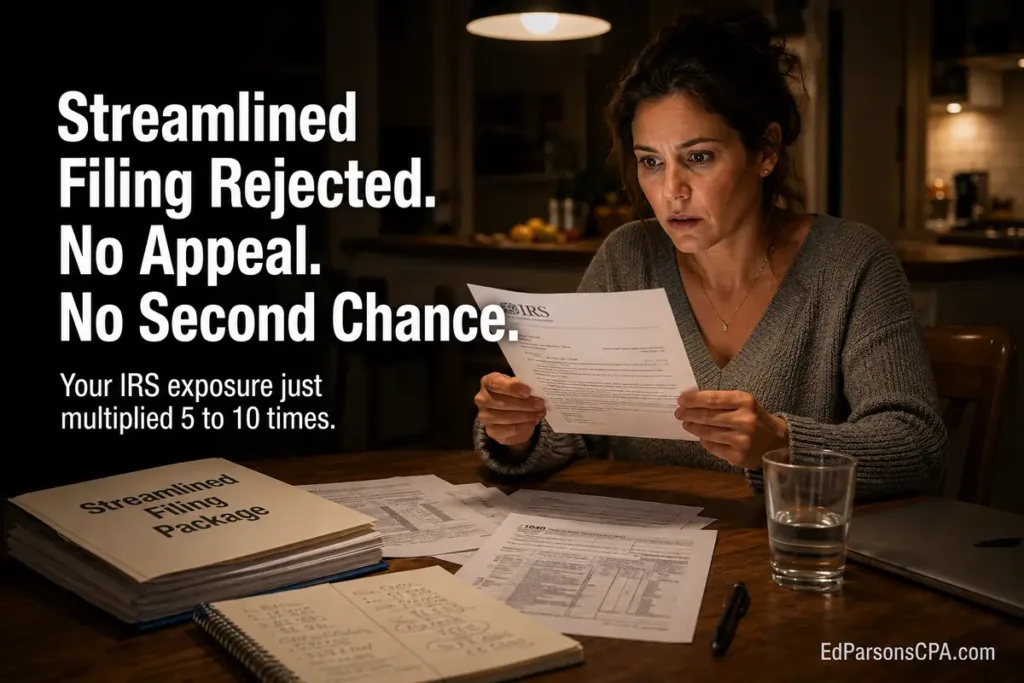

Sara’s streamlined submission was eight months in preparation. The amended returns were filed. The FBARs were corrected. The non-willful certification was signed. She expected the IRS to accept the submission and close the matter.

Instead, she received a one-page letter. The submission was rejected. No specific reason was given. The streamlined penalty she had calculated, $14,000, was no longer available. Her standard penalty exposure now exceeded $90,000.

Every document she had submitted, including the financial history, the willfulness narrative, and the calculation worksheets, remained with the IRS. There was no path to revise and resubmit. This is what a rejected streamlined filing looks like in practice, and why preparation matters more than most taxpayers realize.

What ‘Rejected’ Actually Means in the Streamlined Program?

Rejection is not a request for additional information. It is a final determination by the IRS that the submission does not meet program requirements. The IRS Streamlined Filing Compliance Procedures page outlines the program but does not provide a formal appeal route once rejection occurs.

When the IRS rejects a streamlined submission, several things happen at once:

- The streamlined penalty reduction is permanently unavailable for the covered assets

- The submission documents remain in IRS possession indefinitely

- The non-willful certification, signed under penalty of perjury, becomes a fact in the file

- The full standard penalty structure applies to every unreported foreign asset

- Examination procedures may begin without further notice

The rejection letter itself is typically brief. The IRS is not required to explain in detail what triggered the determination. This makes diagnosing the failure point after the fact difficult, which is why preparation quality is critical.

Why There Is No Formal Appeal Process?

The Streamlined Filing Compliance Procedures are an administrative program, not a statutory right. Taxpayers do not have a legal claim to streamlined treatment. The IRS offers the program voluntarily and reserves full discretion over eligibility determinations.

This structure has practical consequences:

- No Tax Court review of the rejection decision is available

- No Office of Appeals process applies to the streamlined determination itself

- Reasonable cause arguments are still available but as separate procedures

- Reconsideration requests are not part of the program design

This is significantly different from a rejected Form 14654 being treated as a request for additional information. Once rejected, the program door closes. The taxpayer’s remaining options exist outside the streamlined framework entirely.

The Penalty Difference: Streamlined vs Standard After Rejection

The penalty escalation after rejection depends on which forms were originally missed. Most rejected submissions involve multiple unreported obligations, each carrying its own standard penalty when streamlined relief disappears.

| Measurement | Streamlined Filing Accepted | Streamlined Filing Rejected |

| FBAR penalty | Waived | Up to $10,000 per account per year (non-willful) or 50% per year (willful) |

| Form 8938 penalty | Waived | $10,000 per failure plus continuing penalties |

| Form 3520 penalty | Waived | Greater of $10,000 or 35% of value |

| Statute of limitations | Closed at acceptance | Remains open until all forms filed |

| Appeal rights | Not needed | No formal appeal process |

| IRS retains documents | Filed and processed | All documents stay in IRS possession |

| Criminal exposure | Closed | Remains open in willful cases |

For a typical case combining unreported foreign bank accounts and Form 8938 obligations, the standard penalty exposure after rejection can exceed the streamlined penalty by a factor of five or more. Cases involving PFIC holdings or foreign trust obligations can multiply the escalation further.

What the IRS Does With the Documents You Already Submitted?

This is the part many taxpayers underestimate. A rejected streamlined submission does not return the documents to you. Every page submitted remains in IRS possession and may be used in subsequent proceedings.

Common uses of the submitted documentation after rejection:

- As evidence in a subsequent examination of the same tax years

- As basis for calculating the standard penalty under FBAR, Form 8938, and other applicable rules

- As supporting documentation if the IRS pursues criminal referral in willful cases

- As reference material if the taxpayer later attempts reasonable cause or voluntary disclosure

The non-willful certification narrative is especially significant. A statement signed under penalty of perjury, even one the IRS did not accept, becomes part of the taxpayer’s permanent record. Inconsistencies between that narrative and later representations carry credibility risk.

What Options Remain After a Streamlined Rejection?

The remaining paths after rejection are significantly more demanding than the streamlined program. Each requires more documentation, more legal exposure, and more cost.

- Voluntary Disclosure Practice: The IRS maintains a Voluntary Disclosure Practice managed through Criminal Investigation. This program is more punitive than streamlined and is generally appropriate only for willful cases.

- Reasonable Cause Abatement: Penalty abatement under reasonable cause is available, but the burden of proof rests entirely on the taxpayer. After a rejected streamlined submission, building a reasonable cause argument becomes harder because the IRS already has the non-willful certification on file.

- Delinquent FBAR Procedures: These procedures address late FBAR filings only, without the broader scope of streamlined. They are not appropriate when income tax filings are also at issue.

- Standard Examination Defense: If the IRS opens an examination, the taxpayer is in a defensive posture without the benefit of any preemptive penalty reduction.

None of these paths offer the simplicity or the penalty cap that streamlined filing originally provided. This is why getting the streamlined submission right the first time is the most cost-effective option, not the easiest one.

How to Avoid Streamlined Rejection in the First Place?

Most streamlined rejections come from one of three sources: a weak non-willful narrative, an incorrect track selection between SDOP and SFOP, or penalty calculation errors that the IRS reviewer can recalculate independently.

The protective steps before submission:

- Complete a full residency and abode analysis before selecting SDOP or SFOP

- Build the non-willful narrative around specific facts, dates, and supporting documentation

- Reconcile the asset list on Form 14653 or Form 14654 against the FBARs and amended returns line by line

- Apply year-end Treasury exchange rates consistently throughout the calculation

- Include every foreign asset type that may belong in the penalty base, not just the obvious ones

- Have a qualified CPA review the entire submission package before any signature is placed

Speak With a CPA Before Your Submission Is Reviewed

A rejected streamlined filing is not a clerical issue. It is a complete loss of penalty protection, with no formal recourse and a permanent record of the non-willful certification in IRS hands. Ed Parsons CPA has 25+ years of experience preparing streamlined submissions, building non-willful narratives that meet IRS standards, and resolving foreign account compliance issues for clients across all 50 states.

If a streamlined submission is in progress or under preparation, the Streamlined Filing CPA Package covers the full submission including the non-willful certification, the penalty calculation, and the documentation reconciliation that determines whether the IRS accepts or rejects the filing.

To discuss your streamlined filing situation directly, or visit the Ed Parsons CPA contact page to schedule a consultation. Streamlined eligibility narrows the moment the IRS contacts you. Acting early protects every option still available.