Skip to content

Skip to content

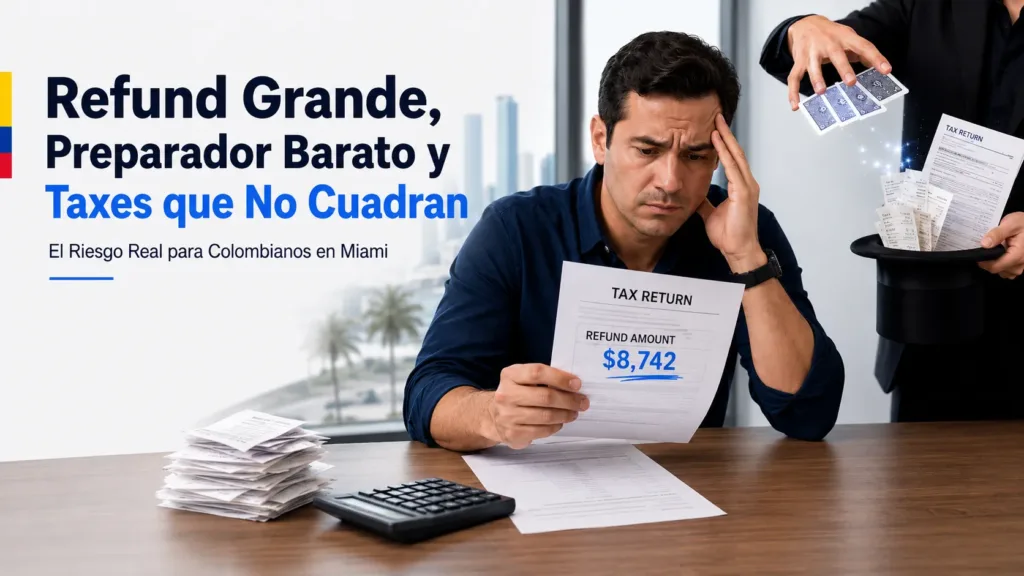

Large Tax Refunds and Cheap Preparers: Risks for Colombians in Miami

Un refund grande se siente bien. Especialmente cuando usted trabaja duro, paga renta, mantiene familia, manda dinero a Colombia, y siente que cada dólar cuenta.

Pero hay una pregunta incómoda que muchos Colombianos en Miami necesitan hacerse:

¿Ese refund fue legítimo, o su preparador hizo “magia” con números que usted no entiende?

Porque en taxes, cuando alguien promete magia, casi siempre hay un truco. Y si el truco aparece en un tax return firmado por usted, el problema no siempre se queda con el preparador.

El IRS ha advertido sobre preparadores que prometen refunds grandes, exageran deductions, reclaman credits para los que el taxpayer no califica, y luego desaparecen después de filing. El taxpayer, mientras tanto, puede quedar con tax due, penalties, interest, audits, or worse.

Este artículo no es para asustarlo sin razón. Es para decirle la verdad: si su refund fue grande porque el preparador inventó gastos, credits, negocios, child care expenses, or deductions que usted no puede explicar, eso sí debe preocuparle.

Y si eso ha pasado año tras año, el riesgo sube.

Cuando el refund parece magia, pregunte cuál fue el truco

Un caso reciente explica perfectamente el problema. El IRS Criminal Investigation reportó que Rafael Alvarez, conocido como “the Magician,” fue sentenciado a prisión por un esquema de tax fraud de aproximadamente $145 million. Según el IRS, el esquema involucró decenas de miles de federal individual income tax returns con información falsa diseñada para reducir fraudulentamente la tax liability de los clientes.

El IRS indicó que esas returns incluían bogus itemized deductions, made-up capital losses, phony business expenses, and fraudulent tax credits. En otras palabras, la “magia” no era magia. Eran números falsos puestos en tax returns reales.

Ese ejemplo importa porque en muchas comunidades el mensaje comercial suena parecido:

“Ven conmigo, yo te saco más refund.”

La pregunta correcta no es solamente cuánto refund le consiguió. La pregunta correcta es:

¿Qué puso en el return para conseguirlo?

Porque el IRS no mira el refund como magia. El IRS mira líneas, schedules, credits, deductions, forms, income, expenses, and signatures.

Fuente: IRS Criminal Investigation report on “the Magician” tax preparer case.

Un refund grande no siempre significa que sus taxes están bien

Un refund grande puede ser completamente legítimo. Puede venir de withholding alto, estimated payments, refundable credits correctamente reclamados, dependents reales, credits válidos, or prior-year corrections.

Pero un refund grande también puede ser una señal de peligro cuando sale de cosas que usted no reconoce:

- Un negocio que usted no tiene.

- Business expenses que usted nunca pagó.

- Mileage falso.

- Child care expenses que no existieron.

- Credits que usted no entiende.

- Dependents que no califican.

- Education credits sin escuela, tuition, or records.

- Charitable deductions inventadas.

- Un preparador que no firmó el return.

El hecho de que el IRS haya aceptado electrónicamente el return no significa que el IRS revisó y aprobó cada número. Muchas veces, el problema llega después: CP2000 notice, audit letter, refund freeze, penalty notice, balance due, or transcript activity.

Si usted ya siente que sus taxes no cuadran, empiece por leer: ¿Tus Taxes No Cuadran? CPA Review para Colombianos en Miami.

Red flags: negocios falsos, gastos inventados y credits que no cuadran

Uno de los trucos más comunes es crear o inflar actividad de negocio. El preparador puede agregar un Schedule C como si usted tuviera un negocio, y luego poner gastos suficientes para reducir income or aumentar un refund.

Eso puede incluir:

- Supplies que usted nunca compró.

- Advertising que nunca pagó.

- Contract labor sin workers reales.

- Business mileage sin records.

- Home office sin calificar.

- Meals, travel, phone, or rent sin soporte.

- Losses de un negocio que no existe.

Si usted no tiene un negocio real, clientes reales, ingresos reales, records reales, and expenses reales, entonces un Schedule C en su return debe levantar una alarma inmediata.

Este es el tipo de “magia” que puede sentirse bien cuando llega el refund, pero puede verse muy diferente cuando el IRS pregunta por los documentos.

Child care expenses: un credit que no se puede inventar

Otro problema común es el child and dependent care credit. Este credit puede ser legítimo, pero no se puede inventar.

Si su return incluye child care expenses, pregúntese:

- ¿Usted realmente pagó daycare or care expenses?

- ¿Tiene recibos?

- ¿Quién fue el provider?

- ¿Tiene nombre, address, and taxpayer identification number del provider?

- ¿El child care fue necesario para que usted pudiera trabajar or buscar trabajo?

- ¿El child or dependent realmente calificaba?

El IRS explica que el child and dependent care credit está relacionado con gastos pagados por el cuidado de una persona qualifying para que el taxpayer pueda trabajar or buscar trabajo. Además, Form 2441 requiere información del care provider y de la persona qualifying.

Fuente oficial: IRS Child and Dependent Care Credit and IRS Form 2441 guidance.

Si usted nunca pagó daycare, no conoce al provider, no tiene records, or el preparador simplemente “lo puso,” eso no es un detalle pequeño. Eso puede convertirse en una pregunta seria del IRS.

Si pasa año tras año, ya no parece accidente

Un error aislado puede ser una cosa. Un patrón de varios años es otra.

Si año tras año usted va al mismo preparador porque “él siempre consigue más refund,” y cada año aparecen gastos que usted no pagó, businesses que usted no tiene, credits que usted no entiende, or child care que nunca ocurrió, el IRS puede mirar más que el preparador.

Puede mirar su conducta.

No basta decir:

“Yo no sabía. El preparador lo hizo.”

Eso puede ser parte de la historia. Pero no necesariamente es toda la defensa.

El problema es que usted firmó el return. Y si durante varios años firmó returns con refunds grandes basados en números que no entendía, no revisó, and could not support, el IRS puede preguntar algo muy simple:

¿Por qué siguió regresando?

Esto es especialmente peligroso cuando los números eran obviamente out of whack. Si usted no tiene negocio, pero hay business expenses. Si usted no pagó child care, pero hay Form 2441. Si usted vive de W-2, pero el return muestra pérdidas de negocio grandes. Si usted tiene un business real que factura bien, pero usa un preparador de $100 que no revisa books, bank statements, payroll, Colombia facts, or records, common sense matters.

La línea entre error, negligence, reckless behavior, and fraud depends on facts. But repeated behavior can look much worse than one mistake.

“Mi preparador lo hizo” no borra su firma

La firma en el tax return importa.

El taxpayer firma bajo penalties of perjury. En palabras simples: usted está diciendo que revisó el return y que, según su conocimiento, está correcto y completo.

Eso no significa que usted no tenga defensa si un preparador actuó mal. Pero sí significa que no debe tratar el problema como si fuera invisible.

El IRS advierte que los taxpayers son legalmente responsables por lo que se presenta, y que un ghost preparer que no firma o no incluye PTIN es un red flag serio. El IRS también dice que los taxpayers nunca deben firmar un blank or incomplete return.

Fuente oficial: IRS warning on ghost preparers and tax credit scams.

Si el preparador no le explicó el refund, no le dio copia completa del return, le dijo que firmara rápido, or no puso su nombre y PTIN como paid preparer, eso es un red flag serio.

Preparador barato, negocio complejo: el smell test importa

Hay returns sencillos. Y hay returns que no son sencillos.

Un W-2 simple con standard deduction puede ser relativamente básico. Pero si usted tiene:

- Business income,

- LLC, corporation, partnership, or payroll,

- Rental property,

- Colombian income,

- Cuentas en Colombia,

- Foreign taxes paid,

- FBAR or Form 8938 issues,

- Pension voluntaria,

- Skandia or Colombian investment funds,

- Property sales in Colombia,

- Foreign corporation or SAS ownership,

then a $100 preparation fee should make you pause.

The issue is not that a low price is automatically illegal. The issue is whether the preparer actually had enough time, training, and documentation to prepare a defensible return.

If the return was cheap, fast, and produced a suspiciously large refund, the question becomes:

Did you buy tax preparation, or did you buy a problem?

If your issue involves a business, entity, payroll, business penalties, or a business refund concern, use the business review route:

Review Business Tax Refund & Risk Assessment

Why PTIN-Only Preparers Lack Full IRS Representation Rights

A paid preparer generally needs a PTIN. But having a PTIN does not make someone a CPA, enrolled agent, attorney, auditor, tax resolution professional, or someone with unlimited authority to represent you before the IRS.

The IRS explains that attorneys, CPAs, and enrolled agents have unlimited representation rights before the IRS. Other preparers may have limited rights or, in some cases, no representation rights beyond preparing the return.

Fuente oficial: IRS preparer credentials and qualifications.

That matters because the person who created the refund may not be able to defend it.

A PTIN-only preparer may be able to prepare a return. That does not mean they can represent you in an audit, analyze penalties, prepare an amended return strategy, handle collection activity, or review complex international issues involving Colombia.

Circular 230: confiar en el cliente no significa cerrar los ojos

A serious tax professional can generally rely on client-provided information in good faith. A CPA or EA is not required to audit every receipt in a normal tax engagement.

But reliance is not blindness.

IRS Circular 230 guidance explains that a practitioner may not ignore other information known to the practitioner and has a duty to make reasonable inquiries if information appears incorrect, incomplete, or inconsistent with other facts or assumptions.

Fuente oficial: IRS Circular 230 and IRS Circular 230 professional responsibility guidance.

That distinction matters.

A professional does not need to treat every client like a criminal. But a professional should not close their eyes when the story does not make sense.

If a taxpayer says they do not have a business, but the preparer creates a Schedule C. If a taxpayer says they did not pay daycare, but Form 2441 appears on the return. If a taxpayer cannot explain a large refund, but the preparer says “no se preocupe,” those are not subtle issues.

That is not normal reliance. That is danger.

El IRS ya conoce estos patrones

This is not just a local rumor. It is a national tax administration problem.

The Government Accountability Office reported that paid preparers file returns for more than half of all taxpayers. GAO also noted that some paid preparers, such as CPAs, have credentials from the IRS or a state, but the majority are not subject to testing or education requirements. GAO further warned that unqualified preparers can make serious errors that may cause taxpayers to lose benefits or become subject to audits or penalties.

Fuente: GAO report on paid tax return preparers.

The Taxpayer Advocate Service has also reported concerns with non-credentialed preparers. In a TAS report discussing paid preparer oversight, TAS stated that among certain paid-preparer EITC returns, 79% were prepared by non-credentialed paid preparers, and over 92% of the audit adjustments in dollars occurred on returns prepared by non-credentialed paid preparers.

Fuente: Taxpayer Advocate Service report excerpt on return preparer oversight.

The IRS also warns about ghost preparers who promise large refunds, exaggerate deductions, claim credits taxpayers do not qualify for, and disappear after filing.

The pattern is known.

Preparers who “make magic” with refunds are not creating money from nowhere. They are putting numbers somewhere on the return.

Why PTIN-Only Preparers Lack Full IRS Representation Rights

Many taxpayers think: “If three years pass, I am safe.”

Sometimes the statute of limitations helps. But it is not a magic shield.

The IRS explains general time limits for assessment, but also explains that if a taxpayer files a false or fraudulent return with intent to avoid tax, the IRS can assess tax for an unlimited amount of time.

Fuente oficial: IRS time limits for assessment.

That is why repeated suspicious refunds matter. If the issue looks like one mistake, the analysis may be different. If the issue looks like a multi-year pattern of fake expenses, fake credits, fake business losses, or returns signed without any support, the conversation changes.

This is why waiting is dangerous. Not every case becomes criminal. Most tax problems are civil. But if you know something is wrong, or should know something is wrong, ignoring it year after year is not a strategy.

Qué revisar antes de que el IRS lo revise por usted

If your refund was large and something feels wrong, do not panic-file an amended return without understanding the facts. But do not ignore it either.

Start by reviewing:

- Your full copy of the filed Form 1040.

- Whether the preparer signed the return and included a PTIN.

- Schedule C, if one appears on the return.

- Business income and business expenses.

- Form 2441, if child care expenses were claimed.

- Education credits, dependents, filing status, and refundable credits.

- Charitable deductions, medical deductions, mileage, and other large expenses.

- IRS transcripts for filing history, refund activity, payments, penalties, and income mismatch clues.

- Prior-year returns to see whether the same pattern happened before.

- Colombia-related facts, including income, accounts, foreign taxes, property, pensions, and business ownership.

IRS transcripts can help identify refund activity, filing gaps, payments, penalties, and mismatch clues. For background, read: How IRS Transcripts Reveal Refunds, Penalties, and Filing Issues.

But if you are Colombian or have Colombia-side facts, transcripts alone may not be enough. Read: Why IRS Transcripts Are Not Enough for Colombian Taxpayers.

Why PTIN-Only Preparers Lack Full IRS Representation Rights

For Colombians in Miami, suspicious refund issues often overlap with international tax issues.

A preparer who did not ask about Colombia may have missed:

- Colombian income,

- DIAN records,

- Foreign taxes paid,

- Form 1116 foreign tax credit issues,

- Colombian bank accounts,

- FBAR,

- Form 8938,

- Rental property in Colombia,

- Sale of property in Colombia,

- Pension voluntaria,

- Skandia or foreign investment funds,

- Colombian SAS or corporation ownership.

If Colombian taxes paid were involved, read: Foreign Tax Credit Mistakes for Colombian Taxes Paid.

If Colombian bank or financial accounts were involved, read: FBAR vs Form 8938 for Colombian Accounts.

A large refund plus missed Colombia facts can mean two problems at the same time: the refund may be wrong, and the international reporting may be incomplete.

Cuándo empezar con CPA Tax Refund & Risk Assessment

If you do not have an active IRS notice yet, but your refund feels wrong, your preparer was sketchy, or you see numbers on your return that you cannot explain, the correct first step may be a CPA-led refund and risk review.

This is especially true if:

- Your refund was unusually large.

- Your preparer promised a refund before reviewing documents.

- Your preparer charged very little for a complex return.

- You see Schedule C activity you do not understand.

- You see child care expenses you did not pay.

- You see credits or deductions you cannot support.

- Your preparer did not ask about Colombia.

- You have multiple years with the same pattern.

Start here:

Start My CPA Refund & Risk Assessment

Si el issue involucra business

If your issue involves an LLC, corporation, partnership, payroll tax, business penalties, business refund risk, entity-level account activity, or a business return that was prepared too cheaply or too quickly, the business route may be more appropriate.

A business return can create more exposure because the records, deductions, income, payroll, and entity facts may be more complex.

Business route:

Review Business Tax Refund & Risk Assessment

Si ya recibió IRS notice, penalty, balance, audit, lien, or levy

If the IRS has already contacted you, this may no longer be a simple refund and risk review.

If you already have:

- IRS notice,

- CP2000,

- audit letter,

- penalty notice,

- balance due,

- lien,

- levy,

- unfiled return issue,

- collection activity,

then the better route may be tax resolution case analysis.

Known IRS problem route:

Start My CPA Refund & Risk Assessment Business Case EvaluationFinal thought: no todo refund grande es malo, pero un refund que no puede explicar merece revisión

A large refund is not automatically wrong.

But a large refund created by a cheap preparer, fake business expenses, child care expenses you did not pay, credits you do not understand, or a pattern that repeats year after year is not something to laugh off.

The preparer may have created the problem. But you signed the return.

If the refund came from “magic,” the IRS may eventually ask what the trick was.

Before that happens, review the return, review the transcripts, identify the risk, and decide whether the return is defensible.

Start with a CPA-led review: