Skip to content

Skip to content

FATCA Compliance Requirements for U.S. Taxpayers Explained

FATCA Compliance Requirements for U.S. Taxpayers Explained: Reporting, Deadlines, and Penalties

By Edward Parsons, CPA, Edward Parsons, CPA

Navigating the complexities of FATCA compliance can be challenging for U.S. taxpayers. The Foreign Account Tax Compliance Act (FATCA) was designed to combat tax evasion by requiring taxpayers to report certain foreign financial assets. This article aims to clarify the specific reporting obligations, submission deadlines, and potential penalties associated with FATCA compliance. It addresses common pain points faced by individuals with foreign assets and the best practices for maintaining compliance. Key sections include a detailed explanation of reporting obligations, important deadlines, and the consequences of non-compliance. Understanding these elements is crucial for effectively managing your tax responsibilities under FATCA.

Reporting Obligations:

Under FATCA, U.S. taxpayers must report foreign financial accounts and other specified assets. The primary reporting form is Form 8938, which is filed with the taxpayer’s annual income tax return. Additionally, if the combined value of foreign accounts exceeds certain thresholds, taxpayers must also submit a Foreign Bank Account Report (FBAR). The specifics of these forms delineate the necessary information and documentation that must be provided to the IRS.

What Are the FATCA Reporting Requirements for U.S. Taxpayers?

Taxpayers are required to disclose specified foreign assets on Form 8938 if their total value exceeds certain thresholds, which vary depending on the taxpayer’s filing status and whether they live in the United States or abroad. This form requires detailed information about each foreign asset, including account numbers, the maximum value during the year, and the name of the financial institution.

Which Foreign Financial Assets Must Be Disclosed under FATCA?

U.S. taxpayers must disclose various foreign financial assets, including:

- Foreign bank accounts: Any account in a foreign financial institution.

- Foreign stocks or securities: Holding stocks or bonds issued by foreign entities.

- Interests in foreign entities: This includes interests in foreign partnerships or corporations.

Understanding what constitutes reportable assets is crucial to ensuring compliance with FATCA.

Submission Deadlines:

FATCA imposes strict deadlines for reporting foreign assets, which often coincide with the taxpayer’s annual tax filing deadlines.

What Are the Key FATCA Deadline Dates U.S. Taxpayers Must Meet?

The key dates for FATCA submission include:

- April 15: The regular deadline for filing tax returns and Form 8938.

- October 15: The extended deadline for those who file for an extension.

Meeting these deadlines is essential to avoid penalties and ensure compliance with IRS regulations.

When Is the Annual Deadline for FATCA Reporting on Form 8938?

The annual deadline for filing Form 8938 is typically April 15 of the following year. Taxpayers living abroad may have a deadline of June 15, with an automatic extension available until October 15, but they must still file Form 8938 by the corresponding dates.

How Do FATCA Deadlines Align with FBAR and Other International Filings?

It is crucial for taxpayers to know that the deadlines for FATCA reporting and FBAR submissions differ. While FBAR must be filed by April 15, there is an automatic extension available until October 15. Taxpayers should ensure that both forms are filed accurately and timely to avoid misalignment that could lead to penalties.

Penalties for Non-Compliance:

Failure to comply with FATCA reporting requirements can result in significant penalties. The IRS has instituted strict enforcement mechanisms to deter non-compliance.

What Are the Potential IRS FATCA Penalties for Non-Compliance?

U.S. taxpayers face various penalties for failing to report foreign accounts or filing inaccurately, including:

- Initial penalties: A failure to file Form 8938 may result in a penalty of $10,000.

- Continuing penalties: If the failure continues after the IRS notifies the taxpayer, penalties can increase significantly, reaching up to $50,000.

- Willful violations: Taxpayers who willfully fail to comply may face steeper penalties, alongside possible criminal charges.

Understanding the potential consequences is vital. For instance, a CP504 notice indicates the IRS’s intent to levy accounts, highlighting the urgency of addressing tax non-compliance.

How Does IRS Enforcement Impact U.S. Taxpayers with Foreign Assets?

The IRS has enhanced its enforcement actions and holds taxpayers accountable for non-compliance through audit processes and investigations into foreign financial disclosures. Taxpayers should be diligent in adhering to their reporting obligations to mitigate the risk of severe penalties.

How Does FATCA Relate to FBAR, PFIC, and CFC Reporting Obligations?

FATCA requirements intersect with various other reporting obligations, such as the FBAR, which is specifically focused on foreign bank accounts, and reporting for Passive Foreign Investment Companies (PFICs) and Controlled Foreign Corporations (CFCs). U.S. taxpayers must be aware of the distinctions and similarities in filing requirements among these regulations. Failing to comply can lead to significant issues, including potential FBAR penalties, especially if filing is delinquent.

Additional Considerations:

When navigating FATCA compliance, it’s essential for taxpayers to understand additional factors that may impact their obligations.

How Does IRS Enforcement Impact U.S. Taxpayers with Foreign Assets?

Beyond penalties, the implications of IRS enforcement can extend to increased scrutiny of a taxpayer’s global financial activities and potential audits. Engaging with a tax professional can be beneficial to ensure all obligations are met accurately. Failure to address IRS notices promptly can lead to severe actions such as a federal tax lien, impacting credit and property.

When Should U.S. Taxpayers Seek Professional Compliance Reviews?

Taxpayers should consider seeking professional compliance reviews if they have substantial foreign financial assets or complex tax scenarios. Consulting a tax professional can help navigate the intricacies of FATCA and reduce the risk of penalties.

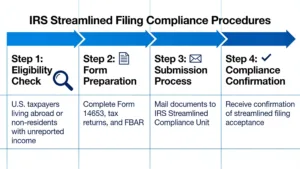

How Do Streamlined Filing Procedures Assist in Delinquent FATCA Compliance?

Streamlined filing procedures offer a way for U.S. taxpayers who failed to file their required forms to come into compliance without facing the harshest penalties. These procedures are particularly useful for those who may have inadvertently failed to report or misunderstood their obligations.

How Can Taxpayers Stay Informed About FATCA Updates and IRS Guidance?

Remaining informed about changes in FATCA regulations and IRS guidance is vital for compliance. Taxpayers can utilize resources such as IRS publications, financial advisory services, and professional networks to keep abreast of updates.

What Resources Provide the Latest FATCA Reporting Rules and Changes?

Taxpayers should direct their attention to official IRS publications, financial institutions, and professional tax advisory services to access the latest information on FATCA reporting rules and updates. Staying educated helps mitigate compliance risks and ensure adherence to current laws.

How Does Ongoing Monitoring of FATCA Enforcement Trends Benefit Taxpayers?

By monitoring trends in FATCA enforcement, U.S. taxpayers can gain insights into potential areas of risk and compliance challenges. Understanding enforcement focuses can guide taxpayers in aligning their financial activities with regulatory expectations and adjusting their reporting practices accordingly. If facing imminent IRS action, understanding the final notice before levy is critical, as detailed in the LT11 Letter 1058 guide.

The consolidated understanding of these reporting aspects underscores the importance of maintaining compliance with FATCA. Taxpayers should stay vigilant about these requirements to protect themselves from potential penalties while ensuring their financial obligations are met.