Skip to content

Skip to content

You have cuentas en Colombia, and now you are seeing two terms everywhere: FBAR and Form 8938.

They sound similar. They both involve foreign accounts or foreign assets. They both can matter for Colombian taxpayers in Miami. But they are not the same form, they are not filed the same way, and filing one does not automatically satisfy the other.

That is where many taxpayers get confused.

A Colombian checking account, savings account, brokerage account, investment account, pension voluntaria, or account connected to Colombian rental property may create more than one question. The issue is not only whether the account earned interest. The issue may involve account value, ownership, signature authority, income, where the form is filed, and whether the taxpayer meets a reporting threshold.

If you need the broader account overview first, read the parent education article: Colombian Bank and Other Financial Accounts, FBAR, and Form 8938.

Quick Answer:

FBAR and Form 8938 are separate foreign account and foreign asset reporting rules. FBAR is filed with FinCEN and generally applies when a U.S. person has foreign financial accounts exceeding $10,000 in aggregate at any time during the year. Form 8938 is filed with the IRS as part of the income tax return and applies to specified foreign financial assets above higher thresholds. Some Colombian taxpayers may need FBAR, Form 8938, both, or neither, depending on the facts. FinCEN states that FBAR applies when the aggregate value of foreign financial accounts exceeds $10,000, while the IRS states that Form 8938 applies when specified foreign financial assets exceed the applicable threshold.

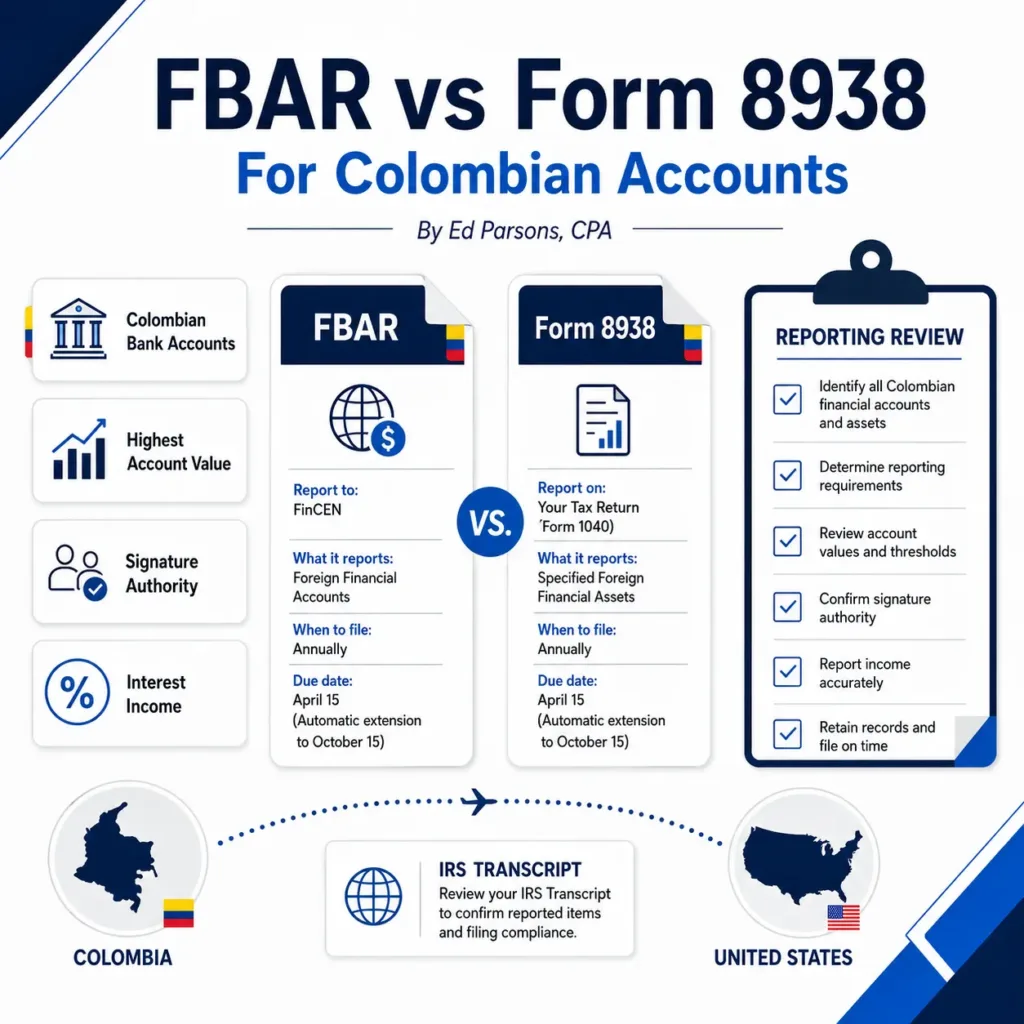

The Simple Difference Between FBAR and Form 8938

The simplest way to understand the difference is this:

FBAR is a foreign financial account report filed with FinCEN.

Form 8938 is an IRS tax return attachment for specified foreign financial assets.

They overlap, but they are not identical. The IRS specifically says that depending on the taxpayer’s situation, a taxpayer may need to file Form 8938, FBAR, or both, and certain foreign accounts may need to be reported on both forms.

That means a Colombian account can raise several different questions:

- Is it a foreign financial account?

- Is it a specified foreign financial asset?

- Did the account value exceed the relevant threshold?

- Did the account produce income?

- Was the taxpayer a U.S. person, specified individual, or specified domestic entity?

- Did the taxpayer have ownership or only signature authority?

- Was the account personal, business, pension-related, or investment-related?

This is why “I filed my tax return” is not enough to know whether the foreign account issue was handled correctly.

What FBAR Is Mainly Looking For

FBAR stands for Report of Foreign Bank and Financial Accounts.

FinCEN says a United States person with a financial interest in, or signature authority over, foreign financial accounts must file an FBAR if the aggregate value of foreign financial accounts exceeds $10,000 at any time during the calendar year.

For Colombian taxpayers, FBAR may come up with:

- Colombian checking accounts

- Colombian savings accounts

- Brokerage or investment accounts

- Accounts where you only had signature authority

- Certain foreign pension or retirement-style accounts depending on facts

- Accounts tied to rental property or family financial activity

The important words are aggregate value. The $10,000 threshold is not only one account. Multiple Colombian and foreign accounts may need to be combined.

FBAR is also not filed with your Form 1040. FinCEN explains that FBAR must be filed electronically using the BSA E-Filing System.

What Form 8938 Is Mainly Looking For

Form 8938 is the IRS form used to report specified foreign financial assets when the total value of those assets is more than the applicable reporting threshold.

Form 8938 is different from FBAR in several ways:

- It is filed with the federal income tax return.

- It applies to specified foreign financial assets, not only foreign accounts.

- It has different thresholds.

- It may include foreign financial accounts and other foreign assets.

- It is tied to the taxpayer’s income tax return filing requirement.

The IRS comparison page lists Form 8938 thresholds for specified individuals living in the United States. For unmarried taxpayers and married taxpayers filing separately, the threshold is more than $50,000 on the last day of the tax year or more than $75,000 at any time during the year. For married taxpayers filing jointly, the threshold is more than $100,000 on the last day of the tax year or more than $150,000 at any time during the year.

For Colombians in Miami, those U.S.-resident thresholds are often the starting point. But filing status, asset type, and residency facts still matter.

FBAR vs Form 8938 Comparison Table

| Question | FBAR | Form 8938 |

|---|---|---|

| Filed with | FinCEN | IRS |

| Form name | FinCEN Form 114 | IRS Form 8938 |

| Filed with tax return? | No | Yes |

| Main focus | Foreign financial accounts | Specified foreign financial assets |

| Common Colombian example | Bank or brokerage account in Colombia | Colombian account or other specified foreign financial asset |

| Threshold | Aggregate foreign accounts over $10,000 at any time during the year | Higher thresholds based on filing status and residency |

| Signature authority only | Can matter | Usually different analysis |

| Can overlap? | Yes | Yes |

| One replaces the other? | No | No |

The IRS states that certain foreign financial accounts are reported on both Form 8938 and FBAR, but the information required by each form is not identical and the rules and definitions differ.

Example 1: Colombian Savings Account With a High Balance

Suppose a Colombian taxpayer in Miami has one savings account in Colombia. It did not earn much interest, but the balance exceeded $10,000 during the year.

That may create an FBAR question because FBAR is based on the aggregate value of foreign financial accounts, not only on income earned.

Form 8938 may or may not apply depending on the total value of specified foreign financial assets and the taxpayer’s filing status. The Form 8938 thresholds are generally higher than the FBAR threshold for U.S. residents.

So the account might require FBAR but not Form 8938.

Example 2: Multiple Colombian Accounts Below $10,000 Each

Suppose the taxpayer has three Colombian accounts:

- Account 1: $4,000

- Account 2: $4,500

- Account 3: $3,000

No single account exceeds $10,000. But together, the accounts exceed $10,000.

That is why aggregate value matters for FBAR. A taxpayer can miss FBAR by looking only at each account separately instead of adding all foreign financial accounts together.

Form 8938 may still require a separate threshold analysis.

Example 3: Colombian Brokerage Account or Investment Account

A Colombian brokerage or investment account may raise both FBAR and Form 8938 questions.

It may also raise income tax questions if there were interest, dividends, sales, gains, losses, foreign taxes paid, or investments requiring additional forms.

For U.S. citizens and resident aliens, the IRS says worldwide income generally must be reported, even when the taxpayer is abroad or the income comes from outside the United States.

So the reporting analysis may involve:

- FBAR

- Form 8938

- Income reporting

- Foreign tax credit

- Currency conversion

- Other foreign investment forms, depending on the assets

For Colombian taxes paid, read: Foreign Tax Credit Mistakes for Colombians Filing U.S. Returns.

Example 4: Pension Voluntaria or Colombian Retirement-Style Account

A pension voluntaria can be more complicated than a regular checking account.

The account may need review for:

- Whether it is a foreign financial account

- Whether it is a specified foreign financial asset

- Whether there were contributions

- Whether there were distributions

- Whether there was account growth

- Whether there are underlying investments

- Whether FBAR applies

- Whether Form 8938 applies

Do not assume that a Colombian pension account is automatically ignored because no money was withdrawn. Also do not assume it is treated like a U.S. retirement account.

The IRS Form 8938 Q&A explains that financial accounts maintained by foreign financial institutions may need to be reported on Form 8938 if the taxpayer’s specified foreign financial assets exceed the applicable threshold.

What Colombian Taxpayers Often Get Wrong

The most common mistakes are not always technical calculations. They are assumptions.

Colombian taxpayers in Miami often assume:

- “My tax return was accepted, so FBAR was handled.”

- “My preparer filed Form 1040, so Form 8938 was handled.”

- “The account earned no interest, so nothing is required.”

- “The balance was under $10,000 in each account, so FBAR does not apply.”

- “I filed FBAR, so I do not need Form 8938.”

- “I filed Form 8938, so I do not need FBAR.”

- “The account is just for family expenses.”

- “The account is in Colombia, not the U.S., so it does not count.”

Some of those facts may matter. But none of them should end the analysis automatically.

If your prior preparer never asked about Colombian accounts, account balances, signature authority, or Form 8938, read: Me Prepararon Mal Los Taxes? What Colombianos en Miami Should Check First.

Why This Is Not Only About Bank Accounts

FBAR and Form 8938 can involve more than ordinary checking and savings accounts.

The FBAR filing product catalog for Edward Parsons CPA notes that FBAR review may cover foreign checking, savings, deposit, brokerage, securities accounts, foreign mutual funds or similar pooled funds, certain cash-value insurance or annuity policies, and accounts with signature authority only.

Form 8938 can also include specified foreign financial assets beyond ordinary bank accounts. The Edward Parsons CPA Form 8938 service description includes specified foreign financial asset review, FATCA filing threshold analysis, foreign account and investment classification, maximum value review, currency conversion coordination, and FBAR comparison and overlap review.

That is why a taxpayer should not reduce the question to “Did I have a bank account?” The better question is:

What foreign financial accounts or assets did I have, what was their value, and which reporting rules applied?

What If the Account Produced Income?

If the account produced income, the issue may expand beyond FBAR and Form 8938.

Income may include:

- Interest

- Dividends

- Investment gains

- Rental deposits

- Pension distributions

- Business receipts

- Property sale proceeds

For U.S. citizens and resident aliens, foreign income may need to be reported on the U.S. return. If Colombian tax was paid, the return may also need to consider whether Form 1116 foreign tax credit applies.

For income basics, read: Do Colombians in Miami Need to Report Colombian Income on U.S. Taxes?.

For property activity, read: Colombian Property, Rental Income, and U.S. Tax Return Risk.

Can IRS Transcripts Show Whether FBAR or Form 8938 Was Filed?

IRS transcripts can help with some IRS-side questions, but they may not show the full FBAR picture.

A tax transcript may help review filing history, account activity, refund activity, penalties, wage and income records, and IRS-side mismatch clues. But FBAR is filed with FinCEN, not as part of the Form 1040 package. That means transcript review and foreign account document review are different layers.

The IRS Get Transcript page explains that taxpayers can access tax records including tax return transcripts, tax account transcripts, wage and income transcripts, and verification of non-filing letters.

For the transcript layer, read: How IRS Transcripts Can Reveal Refunds, Penalties, and Filing Problems.

Review, Form Filing, Streamlined Filing, or Tax Resolution?

The right next step depends on what you already know.

This may be a review issue if:

- You are unsure whether FBAR or Form 8938 applied

- Your preparer never asked about cuentas en Colombia

- You filed a return but do not know whether foreign account reporting was handled

- You want to understand the IRS-side record and risk indicators first

- You do not have an active IRS notice or penalty

This may be a form filing issue if:

- You already know FBAR is required and need FinCEN Form 114 prepared

- You already know Form 8938 is required and need it prepared

- You have current-year foreign account reporting to complete

- You know the forms are missing but there is not yet an active IRS case

Edward Parsons CPA has separate CPA-prepared form services for FinCEN Form 114 FBAR Filing for Foreign Financial Accounts and Form 8938 CPA FATCA Filing for Foreign Financial Assets. The product catalog lists the FBAR service as CPA-prepared FinCEN Form 114 for U.S. persons with foreign financial accounts exceeding $10,000 aggregate at any time during the year, and the Form 8938 service as CPA-prepared FATCA foreign asset reporting with threshold and asset classification review.

This may be a streamlined filing issue if:

- You may have missed multiple years of returns or FBARs

- You have foreign accounts, foreign income, foreign pensions, or foreign tax paid

- You need to evaluate whether Streamlined Filing Compliance Procedures may apply

- The facts are non-willful and need eligibility review

Edward Parsons CPA’s IRS Streamlined Filing Compliance Package is positioned for eligible non-willful taxpayers who may have missed returns or FBARs and may involve preparation of three years of U.S. tax returns and six years of FBARs, with Form 1116, Form 8938, Form 8621, Form 5471, or other forms where applicable.

This may already be a tax resolution issue if:

- You received an IRS notice

- You received a penalty notice

- You owe a balance

- You have unfiled returns

- You have an audit, lien, levy, or collection issue

- You received a CP2000-style mismatch notice

If you are still unsure what category applies, start with review and classification before guessing.

Step-by-Step Review for FBAR vs Form 8938 on Colombian Accounts

Do not decide FBAR vs Form 8938 based on a quick Google search or one account balance screenshot.

For Colombian accounts, the safer review sequence is:

- Identify every Colombian and foreign account.

- Determine ownership, joint ownership, and signature authority.

- Determine maximum value during the year.

- Separate bank accounts from investment accounts, pension accounts, and other financial assets.

- Identify whether the accounts produced income.

- Check whether Colombian taxes were paid or withheld.

- Compare FBAR and Form 8938 thresholds separately.

- Review whether IRS transcripts show related return, penalty, or mismatch activity.

- Decide whether this is review, form filing, streamlined filing, or tax resolution.

Then continue through the cluster:

- Colombian Bank and Other Financial Accounts, FBAR, and Form 8938

- Cuentas Bancarias Colombianas y Reportes IRS, FBAR, 8938, FATCA

- Taxes Colombia USA: What Dual Citizens Often Miss

- Common U.S. Tax Return Mistakes for Dual U.S./Colombian Taxpayers

- Foreign Tax Credit Mistakes for Colombians Filing U.S. Returns

- How IRS Transcripts Can Reveal Refunds, Penalties, and Filing Problems

- CPA Tax Return Review for Colombians in Miami

Tranquilo. The goal is not to panic. The goal is to figure out which rule applies before you ignore the account, amend too fast, file the wrong form, or wait for a notice.

FBAR vs Form 8938 for Colombian Accounts: Common Questions

These FAQs help Colombian taxpayers in Miami understand the difference between FBAR and Form 8938 before they ignore the issue, amend too fast, or file the wrong form.

Is FBAR the same as Form 8938?

No. FBAR and Form 8938 are separate reporting rules. FBAR is filed with FinCEN and generally focuses on foreign financial accounts. Form 8938 is filed with the IRS and reports specified foreign financial assets when the taxpayer exceeds the applicable threshold.

For the broader account overview, read Colombian Bank and Other Financial Accounts, FBAR, and Form 8938 .

Official source: IRS comparison of Form 8938 and FBAR requirements

Can I need both FBAR and Form 8938 for Colombian accounts?

Yes. Depending on the facts, some taxpayers may need FBAR, Form 8938, both, or neither. Filing one does not automatically satisfy the other.

If your preparer never asked about cuentas en Colombia, read Me Prepararon Mal Los Taxes? What Colombianos en Miami Should Check First .

Official source: IRS details on reporting foreign bank and financial accounts

What is the FBAR threshold for Colombian accounts?

FBAR generally applies when a U.S. person has a financial interest in, or signature authority over, foreign financial accounts and the aggregate value of those accounts exceeds $10,000 at any time during the calendar year.

If you already know FBAR preparation is needed, review FinCEN Form 114 FBAR Filing for Foreign Financial Accounts .

Official source: FinCEN FBAR guidance

What is the Form 8938 threshold?

For specified individuals living in the United States, Form 8938 thresholds generally depend on filing status. Unmarried taxpayers and married taxpayers filing separately generally use $50,000 at year-end or $75,000 at any time. Married taxpayers filing jointly generally use $100,000 at year-end or $150,000 at any time.

If you already know Form 8938 preparation is needed, review Form 8938 CPA FATCA Filing for Foreign Financial Assets .

Official source: IRS Form 8938 threshold comparison

Does filing FBAR replace Form 8938?

No. Filing FBAR does not automatically replace Form 8938. The forms have different rules, filing systems, definitions, and reporting requirements.

If the account also produced Colombian income, read Do Colombians in Miami Need to Report Colombian Income on U.S. Taxes? .

Official source: IRS FATCA reporting summary for U.S. taxpayers

Does Form 8938 replace FBAR?

No. Form 8938 does not replace FBAR. A taxpayer may still have a separate FBAR obligation even if Form 8938 is filed with the income tax return.

If Colombian taxes were paid on income connected to the account, read Foreign Tax Credit Mistakes for Colombian Taxes Paid .

Official source: IRS FATCA reporting summary for U.S. taxpayers

Do Colombian accounts matter if they earned no interest?

They may. FBAR and Form 8938 can depend on account or asset value, not only whether the account produced interest. Separately, any income the account did earn may still need U.S. tax return review.

If this is part of a larger prior-return concern, read Common U.S. Tax Return Mistakes for Dual U.S./Colombian Taxpayers .

Official source: FinCEN FBAR guidance

Can IRS transcripts show whether FBAR was filed?

IRS transcripts can help with IRS-side issues such as return processing, payments, refunds, balances, and some income records, but FBAR is filed separately with FinCEN. Transcript review and FBAR review are different layers.

For the IRS-side record, read How IRS Transcripts Reveal Refunds, Penalties, and Filing Issues .

Official source: IRS Get Transcript

Should I amend my tax return if I missed FBAR or Form 8938?

Not automatically. First identify what was missed. FBAR, Form 8938, income reporting, foreign tax credit, IRS transcript issues, and prior-year compliance can require different next steps.

If multiple years of returns or FBARs may be missing, review IRS Streamlined Filing Compliance Package By CPA as a possible route only if the facts fit.

Official source: IRS amended return guidance

When should I use a review, FBAR filing, Form 8938 filing, streamlined filing, or tax resolution analysis?

Use a review when you are unsure whether anything is wrong. Use FBAR or Form 8938 filing services when you already know those forms are needed. Consider streamlined filing only when multiple years of returns or FBARs may be missing and the facts fit. Use tax resolution analysis when there is already an IRS notice, balance, penalty, audit, lien, levy, or collection problem.

Personal review: Tax Refund & Risk Assessment (Personal) . FBAR filing: FinCEN Form 114 FBAR Filing . Form 8938 filing: Form 8938 CPA FATCA Filing . Known IRS problem: Personal CPA Tax Resolution Case Analysis .

Official source: IRS choosing a tax professional