Skip to content

Skip to content

You live in Miami. You filed a U.S. tax return. But you also have Colombia in your financial life.

Maybe you earned income in Colombia. Maybe you received rent from an apartment in Medellín, Bogotá, Cali, Cartagena, or Barranquilla. Maybe you have Colombian bank accounts, a pension voluntaria, dividends, interest, business income, or taxes paid to DIAN.

Now the question is simple:

Do Colombians in Miami need to report Colombian income on U.S. taxes?

In many cases, yes. But the better answer is not panic. The better answer is: first identify what type of Colombian income or asset you have, how it connects to your U.S. tax status, and whether the prior return handled it correctly.

If you already filed and now feel unsure, also read the related Awareness article: Me Prepararon Mal Los Taxes? What Colombianos en Miami Should Check First.

Quick Answer:

Colombians in Miami who are U.S. citizens, green card holders, or U.S. resident aliens generally must report worldwide income on a U.S. tax return, including income from Colombia. Colombian wages, business income, rent, pension income, interest, dividends, and property sale gains may need review. Colombian bank accounts and foreign financial assets may also raise FBAR or Form 8938 questions, even when the income was already taxed in Colombia.

The Core Rule: U.S. Tax Residents Generally Report Worldwide Income

The key issue is not whether the money came from Colombia. The key issue is whether you are a U.S. tax person who must report worldwide income.

The IRS says U.S. citizens and resident aliens are subject to tax on worldwide income from all sources and must report taxable income according to the Internal Revenue Code. IRS Publication 54 also explains that U.S. citizens and resident aliens generally have worldwide income subject to U.S. income tax, regardless of where they live.

That means Colombian income may matter even if:

- The money stayed in Colombia

- The income was paid in Colombian pesos

- No U.S. Form 1099 was issued

- The income was already taxed in Colombia

- The preparer never asked about it

- The bank account was outside the United States

This is where many taxpayers get into trouble. They think, “Eso es de Colombia, not U.S.” But for U.S. citizens, green card holders, and U.S. resident aliens, that distinction may not be enough.

What Counts as Colombian Income?

“Colombian income” does not mean only salary.

It may include:

- Salary or wages from a Colombian employer

- Independent contractor income

- Business income

- Rental income from Colombian property

- Pension or retirement distributions

- Interest from Colombian bank accounts

- Dividends from Colombian companies or investments

- Capital gains from selling property or investments

- Airbnb or short-term rental income

- Partnership, company, or entity-related income

- Certain trust, inheritance, or family transfer situations that require review

Not every item is taxed the same way. Not every item creates the same forms. But if you are a U.S. taxpayer and you had ingresos de Colombia, the income should at least be reviewed.

If your concern is Colombian real estate, the next education page in this cluster is Colombian Property, Rental Income, and U.S. Tax Return Risk.

“But I Already Paid Taxes in Colombia”

Paying tax in Colombia does not automatically mean the income disappears from the U.S. return.

The U.S. return may still need to report the income, then determine whether a foreign tax credit, deduction, or other tax rule applies. The IRS foreign tax credit rules generally allow a credit only for certain foreign taxes imposed by a foreign country or U.S. possession, and usually only income, war profits, and excess profits taxes qualify.

For many Colombians in Miami, the issue is not simply whether Colombian tax was paid. The issue is whether the U.S. return handled the Colombian tax correctly.

Common problems include:

- Colombian income was omitted

- Colombian taxes were ignored

- Form 1116 was missing

- The foreign tax credit was calculated incorrectly

- Foreign taxes were deducted when a credit should have been reviewed

- The U.S. return did not match the Colombian documentation

For a deeper education step, read Foreign Tax Credit Mistakes for Colombians filing US Tax returns

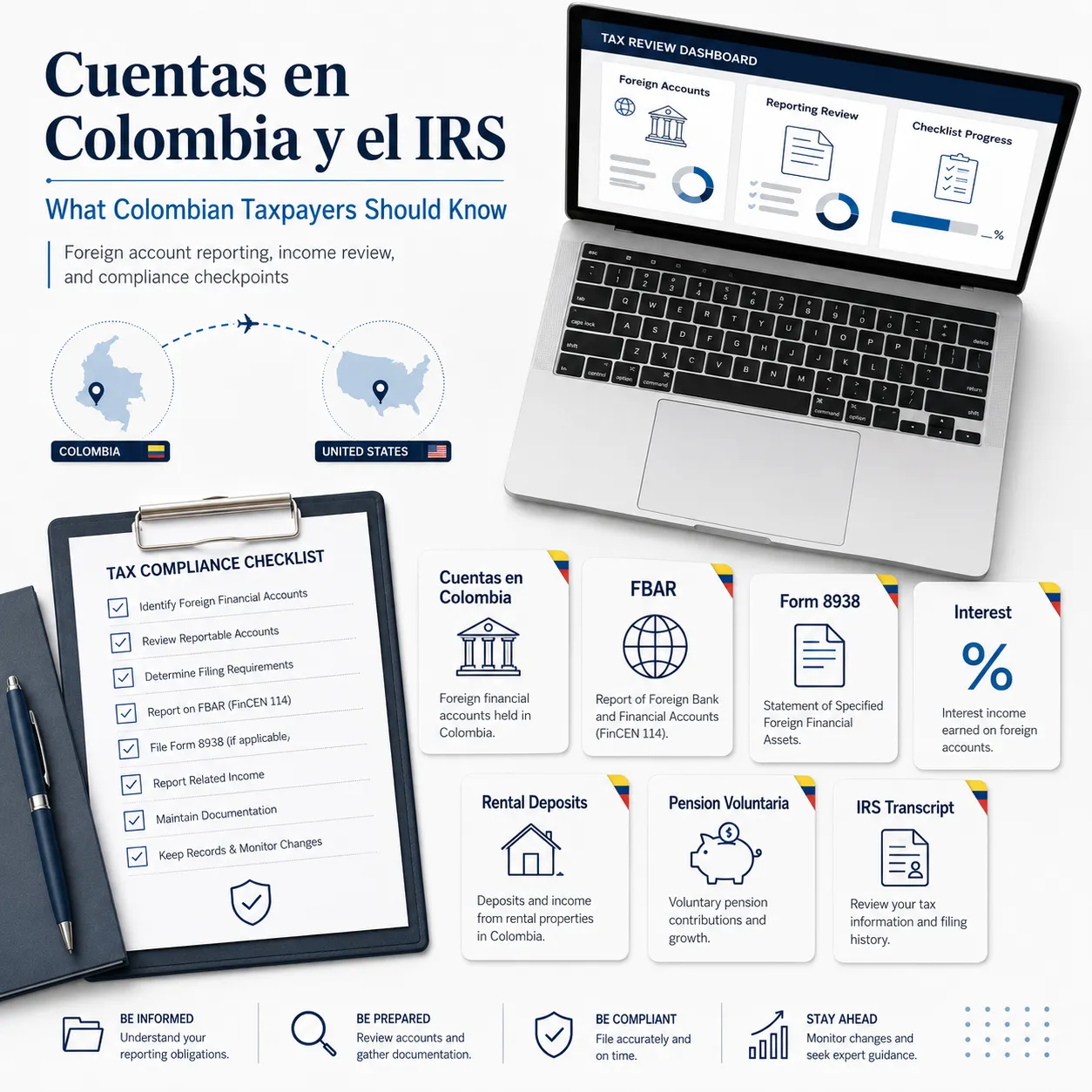

Colombian Bank Accounts Are a Separate Issue

A Colombian bank account is not the same thing as Colombian income.

That matters because a Colombian account can create reporting questions even if the account produced little or no income.

FinCEN says a United States person with a financial interest in, or signature authority over, foreign financial accounts must file an FBAR when the aggregate value of foreign financial accounts exceeds $10,000 at any time during the calendar year.

That means the account balance itself may matter.

Examples include:

- Colombian checking accounts

- Colombian savings accounts

- Investment accounts

- Brokerage accounts

- Accounts with signature authority

- Certain pension or retirement-style accounts depending on facts

Separately, the IRS says Form 8938 is used to report specified foreign financial assets if the total value of those assets is more than the applicable reporting threshold. Filing FBAR does not automatically mean Form 8938 is complete, and filing Form 8938 does not automatically replace FBAR.

For that reason, if your preparer never asked about cuentas en Colombia, read FBAR vs Form 8938 for Colombian Accounts. And Cuentas en Colombia – FBAR

Colombian Pension, Pension Voluntaria, and Retirement Accounts

Colombian pension issues are easy to miss because many taxpayers do not think of a pensión obligatoria, pension voluntaria, or retirement-style account as part of a U.S. tax return.

But the account may need review.

The questions may include:

- Did you receive a pension distribution?

- Was there pension income?

- Were there employee or voluntary contributions?

- Did the account grow during the year?

- Are there underlying investments?

- Was foreign tax paid?

- Does the account create FBAR exposure?

- Does the account create Form 8938 exposure?

Do not assume the answer is automatically yes or no. The U.S. treatment can depend on the account type, taxpayer status, ownership rights, contributions, distributions, and reporting thresholds.

The important point for an Awareness article is simple: if your preparer never asked about pensiones or pension voluntaria, your return may deserve a second look.

Colombian Property and Rental Income

If you own Colombian property, rent it out, or sold it, the U.S. return may need review.

That can include:

- Long-term rental income

- Airbnb or short-term rental income

- Expenses connected to the property

- Depreciation

- Sale proceeds

- Capital gain or loss

- Colombian taxes paid

- Currency conversion

- Ownership structure

- Whether the property belongs to you personally or through an entity

A taxpayer may think, “The apartment is in Colombia, so it does not go on my U.S. return.” That assumption can be risky for U.S. citizens and resident aliens because worldwide income rules may still apply.

For more detail, use the cluster education page: Colombian Property, Rental Income, and U.S. Tax Return Risk.

What If the Income Was Small?

Small does not always mean irrelevant.

A small amount of Colombian interest, rent, dividends, or pension income may still be income. The tax impact might be small, but the reporting question may still matter.

The bigger issue is pattern and documentation.

If Colombian income was ignored for one year, it may have been ignored for several years. If Colombian accounts were never discussed, the return may also have missed FBAR, Form 8938, or interest income. If Colombian taxes were paid, the return may have missed a foreign tax credit review.

This is why the right first step is not panic. It is classification.

Ask:

- What type of income was it?

- Who received it?

- Was I a U.S. citizen, green card holder, or resident alien that year?

- Was it reported on the U.S. return?

- Was tax paid in Colombia?

- Were Colombian accounts or assets involved?

- Did the preparer ask about any of this?

What If the IRS Transcript Does Not Show Colombian Income?

This is an important point.

IRS wage and income transcripts can show information reported to the IRS by U.S. payers, such as Forms W-2 and some Forms 1099. But Colombian-source income may not appear on a U.S. wage and income transcript if no U.S. payer reported it.

That means a clean transcript does not automatically mean Colombian income was handled correctly.

Transcripts are still useful. They can help show IRS-side filing history, refund activity, balances, penalties, payments, and U.S.-reported income. The IRS Get Transcript tool allows taxpayers to access tax return and tax account transcript records.

If your question is “What does the IRS actually show?” the next article to read is How IRS Transcripts Can Reveal Refunds, Penalties, and Filing Problems.

Airbnb en Colombia: no es solo “rental income”

Si usted es U.S. citizen, green card holder, or U.S. resident alien, el income de un Airbnb en Colombia generalmente pertenece en su U.S. tax return aunque el dinero se quede en Colombia, se deposite en Bancolombia, Davivienda, Nequi, una cuenta de administración, or una cuenta de un property manager. El punto de partida es simple: U.S. taxpayers generally report worldwide income. Pero el análisis técnico no termina ahí.

El error común es tratar todo Airbnb como simple Schedule E rental income, o tratarlo automáticamente como Schedule C business income. Ambos tratamientos pueden estar mal si nadie revisó los facts. Real estate rental income is generally reported on Schedule E, but if the owner provides substantial services primarily for the tenant’s convenience, the income and expenses may belong on Schedule C instead.

For short-term rentals, el análisis también puede cruzarse con the passive activity rules. Bajo IRS Publication 925, an activity is not treated as a rental activity for passive activity purposes if the average period of customer use is 7 days or less, or if the average period of customer use is 30 days or less and significant personal services are provided. That matters because an Airbnb in Medellín, Cartagena, Bogotá, or Cali may look like rental real estate economically, but may not behave like a normal passive rental for U.S. tax classification purposes.

The key facts are not just “did Airbnb send money?” The CPA review should look at average stay, guest turnover, cleaning frequency, whether meals, concierge, tours, transportation, laundry, daily cleaning, or other services were provided, who managed the property, whether a property manager acted as agent, whether the taxpayer materially participated, and whether the reporting creates self-employment tax exposure if placed on Schedule C.

Depreciation is another trap. A Colombian Airbnb may require U.S. depreciation tracking in dollars, including building basis, land allocation, improvements, furniture, appliances, placed-in-service dates, and prior depreciation. IRS Publication 946 shows ADS recovery periods, including residential rental property at 30 years under ADS for property placed in service after 2017, with different rules for older property.

Currency conversion also matters. U.S. tax returns are reported in U.S. dollars, so Colombian pesos must be translated into dollars for income, expenses, taxes paid, improvements, platform fees, cleaning, repairs, administración, mortgage interest, and other deductions. The IRS generally refers to using the exchange rate prevailing when the item is received, paid, or accrued, depending on the item and accounting method.

Finally, the Colombian bank accounts connected to the Airbnb can create a separate FBAR and Form 8938 issue. FBAR can apply when a U.S. person has a financial interest in or signature authority over foreign financial accounts and the aggregate value exceeds $10,000 at any time during the year. Form 8938 is a separate IRS reporting regime for specified foreign financial assets; filing one form does not automatically satisfy the other.

For a deeper review of Colombian rental property issues, read Colombian Property, Rental Income, and U.S. Tax Return Risk. If the issue involves Colombian taxes paid, also review Foreign Tax Credit Mistakes for Colombian Taxes Paid. If Airbnb deposits moved through Colombian financial accounts, read FBAR vs Form 8938 for Colombian Accounts.

What If Your Preparer Never Asked About Colombian Income?

That is a red flag, but it does not automatically mean the return was wrong.

Sometimes the preparer made a mistake. Sometimes the taxpayer did not realize Colombia-side facts mattered. Sometimes the intake process was too basic for an international or cross-border situation.

The fair question is:

Did the preparer ask enough to know whether Colombian income, accounts, taxes, pensions, property, or assets mattered?

If the answer is no, the issue may not be the math. The issue may be that important facts never entered the tax return process.

That is exactly why the first article in this cluster focuses on prior preparer doubt: Me Prepararon Mal Los Taxes? What Colombianos en Miami Should Check First.

When This Is a Review Issue vs a Tax Resolution Issue

Not every Colombian income concern is an IRS emergency.

This may be a review issue if:

- You are unsure whether Colombian income was reported

- Your preparer never asked about Colombia

- You want to check refund or risk indicators

- You do not have an active IRS notice

- You want to understand the IRS-side record first

- You are trying to decide whether an amendment may be needed

This may already be a tax resolution issue if:

- You received an IRS notice

- You owe a balance

- You have penalties

- You have unfiled returns

- You have collection activity

- You have a lien, levy, audit, or CP2000-style issue

If this is still a personal return review concern, Edward Parsons CPA offers a CPA-led Tax Refund & Risk Assessment (Personal), which the product catalog describes as an IRS transcript-based review for refund opportunities, penalties, filing issues, and personal tax risks.

If the issue involves a business, LLC, corporation, S corporation, partnership, payroll deposits, or business IRS account activity, the better route may be the Tax Refund & Risk Assessment (Business).

If you already have an IRS notice, balance, penalty, lien, levy, audit, or collection issue, the better route may be Personal CPA Tax Resolution Case Analysis, not a basic review.

Step-by-Step Guide to Reporting Colombian Income on U.S. Returns

If you are asking whether Colombian income belongs on a U.S. tax return, do not guess.

Start by identifying the income category, the account or asset involved, whether Colombian tax was paid, and whether the filed U.S. return addressed those facts. Then compare the filed return with IRS-side records.

For deeper education, continue with these cluster articles:

- How IRS Transcripts Can Reveal Refunds, Penalties, and Filing Problems

- FBAR vs Form 8938 for Colombian Accounts

- Foreign Tax Credit Mistakes for Colombians Filing U.S. Returns

- Colombian Property, Rental Income, and U.S. Tax Return Risk

- CPA Tax Return Review for Colombians in Miami

The goal is not to panic. The goal is to understand what applies before you amend, ignore the issue, or assume everything is fine.

Colombian Income on U.S. Taxes: Common Questions

If you are Colombian in Miami and have ingresos de Colombia, these questions can help you understand what may need review before you amend, ignore the issue, or assume the return was correct.

Do Colombians in Miami need to report Colombian income on a U.S. tax return?

If you are a U.S. citizen, green card holder, or U.S. resident alien, you generally must report worldwide income on your U.S. tax return, including income from Colombia.

If you already filed and are unsure whether your Colombian income was handled correctly, start with the related article Me Prepararon Mal Los Taxes? What Colombianos en Miami Should Check First .

Official source: IRS worldwide income guidance

What types of Colombian income may need to be reported?

Colombian income may include wages, self-employment income, business income, rental income, pension income, dividends, interest, property sale gains, and certain investment income.

If the issue involves Colombian rental property or a property sale, read Colombian Property, Rental Income, and U.S. Tax Return Risk .

Official source: IRS Publication 54

If I paid taxes in Colombia, do I still report the income in the U.S.?

Paying tax in Colombia does not automatically remove the U.S. reporting requirement. The U.S. return may still need to report the income, then evaluate whether a foreign tax credit or deduction applies.

For more detail, read Foreign Tax Credit Mistakes for Colombian Taxes Paid .

Official source: IRS foreign tax credit guidance

Do Colombian bank accounts need to be reported even if they did not earn income?

Possibly. Colombian bank accounts may raise FBAR or Form 8938 questions separate from whether the account produced income. For FBAR, the aggregate value of foreign financial accounts can matter.

Read FBAR vs Form 8938 for Colombian Accounts if your preparer never asked about cuentas en Colombia.

Official source: FinCEN FBAR guidance

What is the difference between Colombian income and Colombian account reporting?

Colombian income is about whether money earned from Colombia belongs on the U.S. tax return. Colombian account reporting is about whether foreign accounts or assets need separate reporting, such as FBAR or Form 8938.

A taxpayer may have one issue, both issues, or neither depending on the facts. The next education article for account reporting is FBAR vs Form 8938 for Colombian Accounts .

Official source: IRS comparison of Form 8938 and FBAR

Does Colombian pension or pension voluntaria income matter?

It can. Colombian pension distributions, retirement-style accounts, and pension voluntaria activity may need review for income tax reporting, FBAR, Form 8938, and foreign tax credit issues.

If this was never discussed with your preparer, the broader trust page ¿Tus Taxes No Cuadran? CPA Review para Colombianos en Miami may be useful after you understand the basic issue.

Official source: IRS taxation of foreign pension and annuity distributions

Will Colombian income show on my IRS transcript?

Not always. IRS wage and income transcripts generally show information reported to the IRS by payers. Colombian income may not appear there if no U.S. payer reported it.

Transcripts can still help reveal IRS-side filing gaps, refund indicators, penalty activity, and mismatch clues. Read How IRS Transcripts Reveal Refunds, Penalties, and Filing Issues .

Official source: IRS Get Transcript

What if my preparer never asked about Colombian income?

That is a reason to take a second look. If the preparer never asked about ingresos de Colombia, cuentas en Colombia, Colombian taxes paid, pensions, rental property, or foreign assets, important facts may have been missed.

Start with Me Prepararon Mal Los Taxes? What Colombianos en Miami Should Check First before deciding whether an amendment or deeper review is needed.

Official source: IRS international individual tax FAQs

Should I amend my return if Colombian income was missed?

Not automatically without review. First, understand what was missed, whether the IRS-side record shows related issues, whether foreign tax credits or account reporting apply, and whether the issue is a simple review matter or an active IRS problem.

If you need to understand the IRS-side record first, read How IRS Transcripts Reveal Refunds, Penalties, and Filing Issues .

Official source: IRS amended return guidance

When should I use a CPA review, business assessment, or tax resolution case analysis?

Use a personal review when the concern is your Form 1040, refund, Colombian income, Colombian accounts, foreign tax credit, or personal IRS transcript. Use a business assessment when the issue involves an LLC, corporation, S corporation, partnership, payroll, business penalties, or business IRS account activity.

For personal return concerns, see Tax Refund & Risk Assessment (Personal) . For business concerns, see Tax Refund & Risk Assessment (Business) . If you already have an IRS notice, balance, penalty, lien, levy, audit, or collection issue, see Personal CPA Tax Resolution Case Analysis .

Official source: IRS preparer credentials and representation rights

{kind=link}